Navigating 2026 Inflation: Strategies to Mitigate Rising Living Costs

Anúncios

The economic landscape is in perpetual motion, and as we look ahead to 2026, forecasts suggest a continued upward trend in the cost of living. A projected 3.5% annual increase in inflation looms, presenting both challenges and opportunities for individuals and households worldwide. Understanding and preparing for this economic reality is not merely a recommendation; it’s a necessity for maintaining financial stability and achieving long-term prosperity. This comprehensive guide, centered around effective 2026 inflation strategies, will delve into the intricacies of inflation, its potential impacts, and actionable steps you can take to mitigate its effects.

Inflation, at its core, is the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. A 3.5% increase might seem modest on paper, but its cumulative effect over time can significantly erode savings, diminish investment returns, and strain household budgets. From daily groceries to housing costs, transportation, and healthcare, every facet of our lives is susceptible to these inflationary pressures. Therefore, developing robust 2026 inflation strategies is paramount to safeguarding your financial future.

Anúncios

The goal of this article is to empower you with the knowledge and tools to not just survive, but thrive in an inflationary environment. We’ll explore various aspects, from understanding the macroeconomic factors driving inflation to implementing personal finance adjustments and exploring savvy investment avenues. By the end of this read, you’ll have a clearer roadmap for navigating the economic currents of 2026 and beyond.

Understanding the Dynamics of 2026 Inflation

Before we dive into specific 2026 inflation strategies, it’s crucial to grasp the underlying mechanisms driving current and projected inflation. Several interconnected factors contribute to inflationary pressures. These include supply chain disruptions, increased consumer demand, expansionary fiscal and monetary policies, and geopolitical events. While some of these factors are global, others might be specific to regional or national economies.

Anúncios

For instance, post-pandemic economic recovery has seen a surge in demand for goods and services, often outstripping the capacity of supply chains to deliver. This imbalance naturally pushes prices upwards. Concurrently, governments and central banks have implemented various stimulus measures to support economies, injecting more money into circulation, which can also devalue currency and fuel inflation. Geopolitical tensions, such as conflicts or trade disputes, can further exacerbate the situation by disrupting energy supplies or raw material availability, leading to higher production costs that are then passed on to consumers.

The projected 3.5% annual increase for 2026 is an average. This means some sectors might experience even higher price hikes, while others might see more moderate increases. Essential goods and services, such as food, energy, and housing, often bear the brunt of inflation, disproportionately affecting lower and middle-income households. Therefore, tailoring your 2026 inflation strategies to address these specific areas of impact is vital.

Economists and financial institutions use various models to forecast inflation, considering historical data, current economic indicators, and future policy expectations. While forecasts can change, a consistent projection of 3.5% suggests a need for proactive measures. Ignoring these signals could lead to a significant erosion of purchasing power and a decrease in real wealth. The time to strategize and implement your defense against rising costs is now, not when the effects are fully felt.

Revisiting and Adjusting Your Personal Budget for 2026

The cornerstone of any effective 2026 inflation strategies begins with a thorough review and adjustment of your personal budget. Inflation directly impacts your monthly expenses, making it imperative to understand where your money is going and identify areas for optimization. This isn’t just about cutting costs; it’s about making smarter financial decisions to preserve your purchasing power.

Start by meticulously tracking all your income and expenses for at least a month, if you aren’t already doing so. Categorize your spending into fixed costs (rent/mortgage, loan payments, insurance) and variable costs (groceries, entertainment, utilities, transportation). Pay particular attention to variable expenses, as these are often where the most significant adjustments can be made.

Analyzing Spending Habits

With a 3.5% increase in living costs, items that once seemed affordable might become a strain. Analyze your spending habits to identify non-essential expenditures that can be reduced or eliminated. This could include subscriptions you rarely use, frequent dining out, or impulse purchases. Consider opting for generic brands over premium ones, especially for groceries and household items, as the quality difference is often negligible but the price savings can be substantial.

Optimizing Essential Services

Even essential services can be optimized. Review your utility bills – electricity, gas, internet, and mobile phone plans. Are you on the most cost-effective plan for your usage? Can you implement energy-saving practices at home? Negotiating with service providers for better rates or switching to more competitive providers can yield significant savings over time. For transportation, explore carpooling, public transport, or optimizing your vehicle’s fuel efficiency to counter rising fuel prices.

Building an Emergency Fund

An emergency fund becomes even more critical in an inflationary environment. Aim to have at least three to six months’ worth of living expenses saved in an easily accessible, high-yield savings account. This fund acts as a buffer against unexpected price hikes or unforeseen financial challenges, preventing you from falling into debt to cover rising costs. Including an emergency fund is a core component of robust 2026 inflation strategies.

Debt Management

High-interest debt, such as credit card debt, becomes more burdensome during periods of inflation. The real cost of borrowing increases, eating into your disposable income. Prioritize paying down these debts aggressively. Consider consolidating high-interest debt into a lower-interest loan if possible. Reducing your debt burden frees up cash flow, which can then be allocated to other inflation-mitigating strategies or savings.

Smart Investment Strategies to Combat Inflation

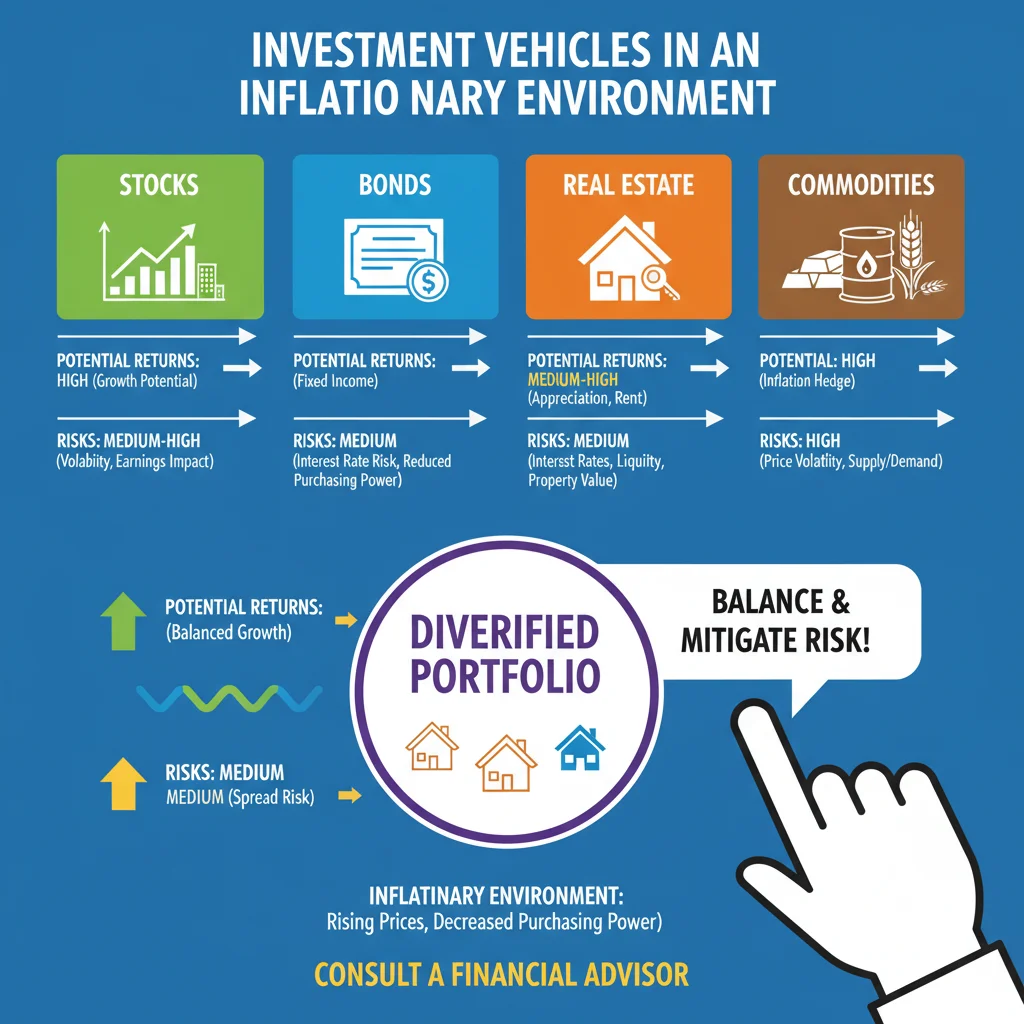

While budgeting helps manage current expenses, smart investment strategies are crucial for preserving and growing your wealth in the face of a projected 3.5% annual increase in living costs. Simply holding cash in a traditional savings account will see its purchasing power erode over time. The key is to invest in assets that traditionally perform well during inflationary periods or offer inflation-hedging qualities. This section will explore various investment avenues that form essential 2026 inflation strategies.

Real Estate

Real estate has long been considered a strong hedge against inflation. Property values and rental income tend to increase with inflation, as the cost of building new properties rises, making existing ones more valuable. If you own property, consider if your rental income is keeping pace with inflation. For potential homeowners, while mortgage rates might fluctuate, the long-term appreciation of real estate can outweigh the initial costs. Investing in REITs (Real Estate Investment Trusts) can also offer exposure to real estate without direct property ownership.

Inflation-Protected Securities (TIPS)

Treasury Inflation-Protected Securities (TIPS) are bonds issued by the U.S. Treasury that are indexed to inflation. Their principal value adjusts with the Consumer Price Index (CPI), meaning your investment grows with inflation, and your interest payments are based on this adjusted principal. TIPS are one of the most direct ways to hedge against inflation and should be a consideration in your 2026 inflation strategies, especially for conservative investors.

Commodities

Commodities like gold, silver, oil, and other raw materials often perform well during inflationary times. As the cost of goods rises, so does the value of the raw materials used to produce them. Gold, in particular, is often seen as a safe haven asset during economic uncertainty and inflationary pressures. You can invest in commodities directly, through commodity ETFs, or via futures contracts, though direct commodity investment can be volatile and requires careful consideration.

Stocks of Companies with Pricing Power

Not all stocks are equal when it comes to inflation. Companies that have strong pricing power – meaning they can raise their prices without significantly impacting demand for their products or services – tend to fare better. These are often established companies with strong brands, essential products, or dominant market positions. Look for businesses with high-profit margins and low debt levels, as they are better positioned to absorb rising costs and pass them on to consumers. Diversifying your stock portfolio with such companies is a smart move for your 2026 inflation strategies.

Dividend Stocks

Investing in dividend-paying stocks can provide a steady stream of income that can help offset the rising cost of living. Companies that consistently pay and ideally increase their dividends can offer a form of inflation protection, as your income stream grows over time. Focus on companies with a strong history of dividend growth and healthy balance sheets.

Diversification is Key

No single investment is a silver bullet against inflation. A diversified portfolio that includes a mix of these assets is generally the most prudent approach. Spreading your investments across different asset classes reduces risk and increases the likelihood that at least some parts of your portfolio will perform well in an inflationary environment. Regularly review and rebalance your portfolio to ensure it remains aligned with your financial goals and risk tolerance.

Protecting Your Income and Enhancing Earning Potential

While managing expenses and making smart investments are crucial, enhancing your income and protecting its purchasing power are equally vital components of effective 2026 inflation strategies. In an environment where costs are rising, increasing your earning potential can provide a significant buffer.

Negotiating Salary and Raises

Don’t shy away from negotiating your salary or asking for a raise. As the cost of living increases, so too should your compensation. Research industry benchmarks for your role and skills, and be prepared to articulate your value to your employer. Regular performance reviews are ideal times to discuss salary adjustments. If your current employer isn’t willing to offer a raise commensurate with inflation, it might be time to explore other opportunities.

Upskilling and Reskilling

Investing in your own human capital is one of the best long-term 2026 inflation strategies. Acquire new skills or refine existing ones that are in high demand in the job market. This not only makes you more valuable to your current employer but also opens doors to higher-paying roles or new career paths. Online courses, certifications, and workshops are accessible ways to boost your professional value. The more specialized and in-demand your skills, the greater your leverage in salary negotiations.

Exploring Side Hustles and Passive Income

A side hustle can provide an additional stream of income that helps offset inflationary pressures. This could be anything from freelancing in your area of expertise, driving for a ride-sharing service, selling handmade crafts, or tutoring. Passive income streams, such as investing in dividend stocks (as mentioned earlier), creating digital products, or renting out a spare room, can also provide a valuable financial cushion with less active effort once established.

Reviewing and Optimizing Benefits

Beyond your base salary, thoroughly review your employee benefits package. Are you maximizing your 401(k) contributions, especially if there’s an employer match? This is essentially free money and compounds over time, helping to outpace inflation. Explore health savings accounts (HSAs) if available, as they offer tax advantages for healthcare costs, which are also susceptible to inflation. Understanding and utilizing all available benefits can significantly boost your overall financial health.

Considering Geographic Arbitrage

For some, a more drastic but potentially impactful strategy could be geographic arbitrage. If your job allows for remote work, consider relocating to an area with a lower cost of living while maintaining your current salary. The difference in housing, taxes, and general expenses can be substantial, effectively increasing your disposable income without a pay raise. This requires careful planning but can be a powerful counter-inflationary move.

Lifestyle Adjustments for a High-Inflation Environment

Beyond financial planning and investment, certain lifestyle adjustments can play a significant role in mitigating the impact of inflation. These are practical, everyday changes that can collectively lead to substantial savings and improved financial resilience, complementing your broader 2026 inflation strategies.

Mindful Consumption

Adopt a mindset of mindful consumption. Before making a purchase, ask yourself if it’s truly a need or a want. Can you repair an item instead of replacing it? Can you borrow or rent instead of buying? Reducing overall consumption not only saves money but also has environmental benefits. This shift in perspective can lead to long-term savings and a more sustainable lifestyle.

Energy Efficiency at Home

Energy costs are often a major driver of inflation. Invest in energy-efficient appliances, seal drafts in your home, optimize your thermostat settings, and use natural light whenever possible. Small changes like unplugging electronics when not in use or switching to LED lighting can add up to significant savings on your utility bills over the year. Government incentives for energy-efficient home improvements can also make these investments more affordable.

Meal Planning and Bulk Buying

Food prices are particularly susceptible to inflation. Strategic meal planning, cooking at home more often, and buying in bulk for non-perishable items can significantly reduce your grocery bill. Look for sales, use coupons, and consider growing some of your own produce if feasible. Reducing food waste is another powerful way to save money, as wasted food is wasted money.

Rethinking Transportation

With rising fuel costs, re-evaluating your transportation habits is essential. If possible, walk, bike, or use public transportation for shorter commutes. Carpool with colleagues or friends. If you own a car, ensure it’s well-maintained to maximize fuel efficiency. For long-term considerations, an electric vehicle might be a compelling option, especially with government incentives, though the initial investment needs to be weighed against potential fuel savings.

DIY and Home Maintenance

Labor costs for services are also subject to inflationary pressures. Learning basic DIY skills for home maintenance and repairs can save you considerable money. From fixing a leaky faucet to painting a room, tackling these tasks yourself can prevent expensive service calls. Utilize online tutorials and resources to build your practical skills.

The Role of Technology in Mitigating Inflation

In the age of digital transformation, technology offers numerous tools and platforms that can be integrated into your 2026 inflation strategies. Leveraging these innovations can enhance your ability to save, invest, and manage your finances more effectively.

Budgeting Apps and Software

Modern budgeting apps like Mint, YNAB (You Need A Budget), or Personal Capital can automate the tracking of your income and expenses, provide real-time insights into your spending patterns, and help you stick to your financial goals. Many offer categorization features, bill reminders, and even investment tracking, making financial management much more streamlined.

Robo-Advisors for Investment

For those new to investing or looking for a hands-off approach, robo-advisors such as Betterment or Wealthfront can be invaluable. These platforms use algorithms to manage your investment portfolio based on your financial goals and risk tolerance, often at a lower cost than traditional financial advisors. They can help you build diversified portfolios that include inflation-hedging assets, making them a smart component of your 2026 inflation strategies.

Price Comparison Tools and Apps

Before making any purchase, especially for larger items, utilize price comparison websites and apps. Tools like Google Shopping, CamelCamelCamel (for Amazon), or browser extensions like Honey can help you find the best deals, track price drops, and apply coupons automatically. This ensures you’re always getting the most value for your money, directly combating rising prices.

E-commerce and Online Marketplaces

Online shopping can offer more competitive pricing due to lower overheads for sellers. Furthermore, online marketplaces for used goods (e.g., eBay, Facebook Marketplace, Craigslist) can be excellent resources for finding items at a fraction of their new cost, or for selling items you no longer need to generate extra income.

Financial Literacy Platforms

The internet is a vast repository of financial information. Utilize reputable financial blogs, podcasts, and online courses to continuously educate yourself on personal finance, investment strategies, and economic trends. The more informed you are, the better equipped you will be to adapt your 2026 inflation strategies to changing circumstances.

Consulting Financial Professionals

While this article provides a broad overview of 2026 inflation strategies, every individual’s financial situation is unique. For personalized advice and tailored planning, consulting a qualified financial advisor can be incredibly beneficial. A professional can help you:

- Assess Your Current Financial Health: Gain a clear picture of your assets, liabilities, income, and expenses.

- Develop a Personalized Plan: Create a financial plan that aligns with your specific goals, risk tolerance, and time horizon, factoring in inflationary pressures.

- Optimize Investment Portfolios: Receive expert guidance on asset allocation and specific investment vehicles best suited for an inflationary environment.

- Tax Planning: Understand how inflation might impact your tax obligations and identify strategies to minimize your tax burden.

- Estate Planning: Ensure your long-term wealth transfer plans are inflation-proof.

When choosing a financial advisor, look for one who is a fiduciary, meaning they are legally obligated to act in your best interest. Interview several advisors to find one whose philosophy and approach resonate with your needs. The cost of professional advice can be a worthwhile investment, especially when navigating complex economic periods like projected high inflation.

Conclusion: Proactive Steps for a Secure 2026

The projected 3.5% annual increase in living costs by 2026 is a significant economic forecast that demands attention and proactive planning. Ignoring these signals could lead to a tangible reduction in your purchasing power and financial well-being. However, by implementing a combination of well-thought-out 2026 inflation strategies, you can not only mitigate the negative impacts but potentially even strengthen your financial position.

The journey to financial resilience in an inflationary environment begins with a clear understanding of your current financial standing, followed by disciplined budgeting and smart spending. It extends to strategic investments in assets that historically perform well during inflation, and continuously seeking opportunities to enhance your income and professional value. Finally, making conscious lifestyle adjustments and leveraging technological tools can provide additional layers of protection and efficiency.

Remember, inflation is a persistent economic force, but it is not an insurmountable one. By taking a proactive, informed, and adaptive approach, you can navigate the economic landscape of 2026 with confidence, ensuring your financial future remains secure and prosperous. Start today by reviewing your finances, setting clear goals, and incrementally implementing these strategies. Your future self will thank you for the foresight and effort.

and IRA Contributions")