Mastering Personal Budgeting in 2026: The 50/30/20 Rule for Financial Stability Amidst Inflation

Anúncios

Mastering Personal Budgeting in 2026: The 50/30/20 Rule for Financial Stability Amidst Inflation

As we navigate the complexities of modern economics, the year 2026 presents its own unique set of challenges and opportunities for personal finance. With persistent inflationary pressures and an ever-evolving global financial landscape, effective personal budgeting 2026 is not just a recommendation; it’s a necessity. This comprehensive guide will equip you with the knowledge and strategies to not only survive but thrive financially by expertly applying and adapting the renowned 50/30/20 rule.

The concept of personal budgeting has been around for decades, yet its application must continually evolve to remain relevant. What worked perfectly in 2020 might fall short in 2026, especially when faced with the relentless erosion of purchasing power due to inflation. Understanding these dynamics and proactively adjusting your financial habits are paramount to achieving and maintaining financial stability.

Anúncios

This article delves deep into the core principles of the 50/30/20 rule, offering practical insights into how to customize it for your specific circumstances in 2026. We will explore how to accurately categorize your expenses, identify areas for optimization, and implement strategies to protect and grow your wealth in an inflationary environment. Whether you’re a seasoned budgeter or just starting your financial journey, the information presented here will provide a robust framework for your success.

The goal is not merely to track where your money goes but to strategically allocate it in a way that aligns with your financial aspirations, mitigates risks, and builds a resilient financial future. Let’s embark on this journey to master personal budgeting 2026 together.

Anúncios

Understanding the Economic Landscape of 2026: Why Budgeting is More Crucial Than Ever

Before diving into the mechanics of budgeting, it’s essential to grasp the economic backdrop against which we’re operating. The year 2026 is projected to continue experiencing the ripple effects of global economic shifts, supply chain disruptions, and geopolitical events. Inflation, in particular, remains a significant concern, impacting everything from groceries and housing to transportation and discretionary spending. This continuous increase in the cost of living means that the same amount of money buys less than it did before, making thoughtful financial planning indispensable.

The Persistent Threat of Inflation

Inflation is not just an abstract economic term; it’s a tangible force that directly affects your daily life and long-term financial goals. When inflation is high, your savings lose value, and your income’s purchasing power diminishes. This makes saving for retirement, a down payment on a house, or even a simple vacation significantly more challenging. For personal budgeting 2026 to be effective, it must explicitly address and counteract the effects of inflation.

Understanding the causes of inflation – whether demand-pull, cost-push, or built-in – can help you anticipate future trends and make more informed financial decisions. Monitoring economic indicators, staying updated on central bank policies, and understanding how these factors influence market prices are crucial steps in preparing your budget for the realities of 2026.

The Importance of Financial Resilience

Beyond inflation, other economic uncertainties such as potential recessions, job market fluctuations, and interest rate changes can destabilize even the most carefully laid financial plans. Building financial resilience through robust personal budgeting 2026 means having an emergency fund, managing debt responsibly, and diversifying your investments. It’s about creating a financial buffer that can absorb unexpected shocks without derailing your long-term objectives.

A resilient budget is one that is flexible enough to adapt to changing circumstances. It’s not a rigid set of rules but a dynamic framework that allows for adjustments based on economic realities and personal life events. This adaptability is a cornerstone of successful budgeting in an unpredictable world.

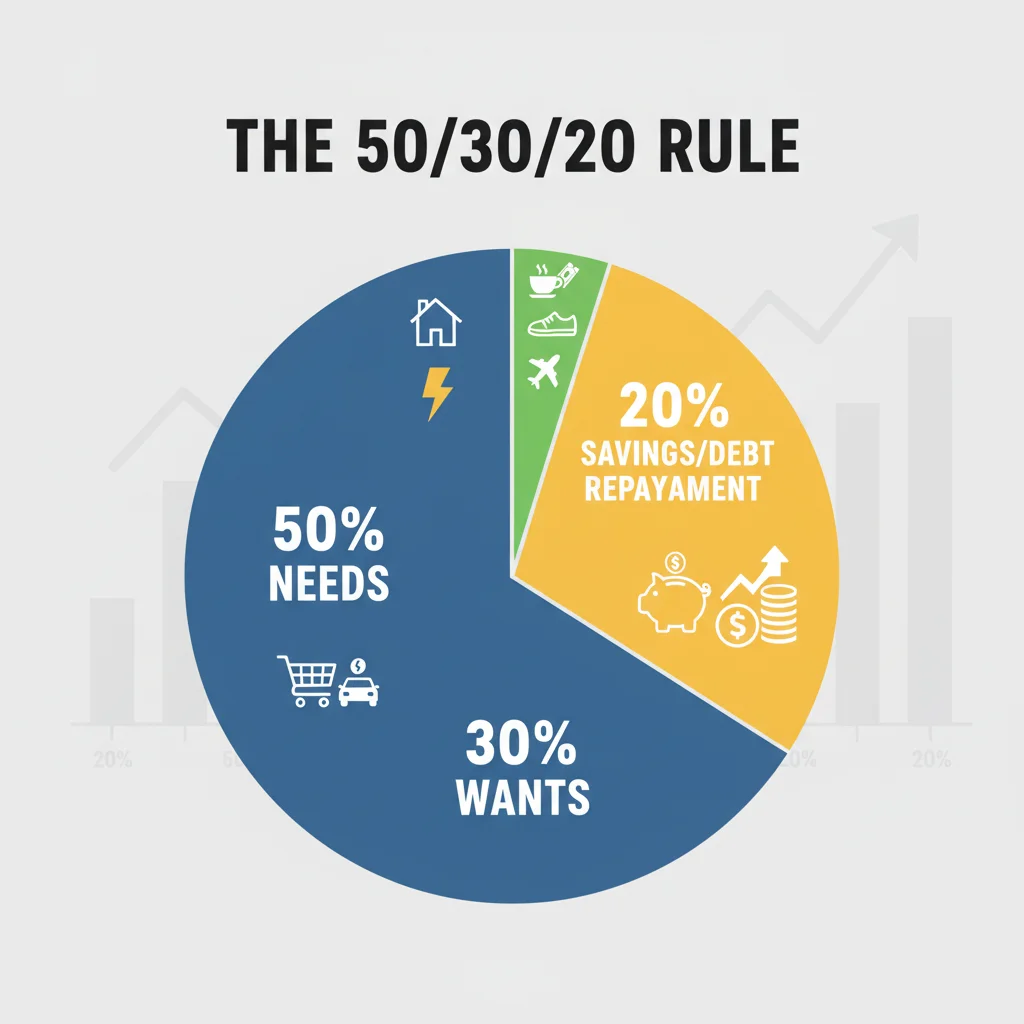

The 50/30/20 Rule Revisited: A Foundation for Modern Budgeting

The 50/30/20 rule is a popular and straightforward budgeting guideline that suggests allocating your after-tax income as follows: 50% to Needs, 30% to Wants, and 20% to Savings and Debt Repayment. While simple, its effectiveness lies in its clarity and flexibility. However, for personal budgeting 2026, we need to delve deeper into its application and consider how inflation and other economic factors might necessitate adjustments.

50% for Needs: The Essentials of Life

Your ‘Needs’ category encompasses all the essential expenses required for survival and maintaining your current lifestyle. This typically includes:

- Housing: Rent or mortgage payments, property taxes, home insurance.

- Utilities: Electricity, water, gas, internet.

- Groceries: Essential food items.

- Transportation: Car payments, insurance, fuel, public transit.

- Healthcare: Insurance premiums, necessary medical expenses.

- Minimum Debt Payments: The minimum required payments on credit cards, student loans, etc. (note: any payments above the minimum go into the 20% category).

In an inflationary environment, the cost of these needs can escalate rapidly. What constituted 50% of your income last year might now be 60% or more. This is where the adaptability of your personal budgeting 2026 comes into play. You might need to scrutinize these categories more closely to find areas for reduction, or you might need to adjust the percentages of the rule itself.

30% for Wants: Enhancing Your Life

The ‘Wants’ category includes all the expenses that improve your quality of life but are not strictly necessary. These are often the first areas to cut back on when inflation tightens your budget. Examples include:

- Dining out and takeout.

- Entertainment (movies, concerts, streaming services).

- Hobbies and leisure activities.

- Vacations and travel.

- New clothes and accessories (beyond basic necessities).

- Gym memberships (if not considered essential for health).

This category offers the most flexibility for adjustment. If your ‘Needs’ section creeps above 50% due to inflation, the ‘Wants’ category is where you’ll likely need to make significant concessions. Prioritizing which ‘wants’ bring the most value and cutting back on others is a key strategy for effective personal budgeting 2026.

20% for Savings & Debt Repayment: Building Your Future

This crucial category is dedicated to securing your financial future. It includes:

- Emergency Fund: Ideally three to six months of living expenses.

- Retirement Savings: Contributions to 401(k), IRA, or other retirement accounts.

- Investment Accounts: Brokerage accounts for long-term growth.

- Debt Acceleration: Payments above the minimum on credit cards, student loans, or mortgages to pay them off faster.

- Specific Savings Goals: Down payment for a house, car, education, etc.

In an inflationary period, maintaining this 20% allocation can be challenging but is more vital than ever. Inflation erodes the value of cash, making investments that can outpace inflation even more critical. Prioritizing high-interest debt repayment also becomes more urgent as interest rates may rise in response to inflation, increasing the cost of borrowing.

Adapting the 50/30/20 Rule for Inflation in 2026

The beauty of the 50/30/20 rule is its adaptability. It’s a guideline, not a rigid law. In 2026, with inflation as a significant factor, you might find that a strict 50/30/20 split is unrealistic or suboptimal. Here’s how to adapt it for maximum effectiveness in your personal budgeting 2026 efforts:

Re-evaluating Your Needs: The Inflationary Squeeze

The first step is to meticulously re-evaluate your ‘Needs’ category. Due to inflation, the cost of housing, groceries, and utilities may have increased significantly. Track these expenses diligently for a month or two to get an accurate picture. If your needs now exceed 50% of your income, you have a few options:

- Reduce Wants: This is often the easiest and most immediate solution. Cut back on discretionary spending to free up funds for essential needs.

- Increase Income: Explore opportunities for a raise, a side hustle, or a second job to boost your overall income.

- Optimize Needs: Can you find a cheaper apartment, carpool to save on transportation, or switch to a more affordable grocery store? Even small changes can add up.

- Adjust Percentages: In extreme cases, you might temporarily shift to a 60/20/20 or even 55/25/20 model, where ‘Needs’ take a larger share, and ‘Wants’ are further reduced. The key is to protect your savings and debt repayment portion as much as possible.

Strategic Management of Wants: Smart Spending

Managing your ‘Wants’ effectively in 2026 means being a smart consumer. Instead of outright eliminating all wants, look for ways to enjoy them more affordably. For example, instead of dining out frequently, try cooking at home more often or opting for lunch specials. Consider free or low-cost entertainment options. Subscribing to fewer streaming services or sharing subscriptions can also free up significant funds.

The goal here is not deprivation but conscious spending. Every dollar saved from your ‘Wants’ category can be redirected to ‘Needs’ if they’ve inflated, or, ideally, to ‘Savings and Debt Repayment’ to accelerate your financial goals. This conscious approach is vital for effective personal budgeting 2026.

Prioritizing Savings and Debt Repayment Amidst Inflation

This 20% category is your shield against inflation and your engine for wealth creation. When inflation is high, the real value of your cash savings diminishes. Therefore, it’s crucial to:

- Maximize High-Yield Savings Accounts: Ensure your emergency fund and short-term savings are in accounts that offer the highest possible interest rates to somewhat offset inflation.

- Invest Smartly: Consider investments that historically perform well during inflationary periods, such as inflation-protected securities (TIPS), real estate, commodities, or dividend-paying stocks. Diversification is key.

- Aggressively Pay Down High-Interest Debt: Credit card debt, in particular, can become a significant drain when interest rates rise. Paying it down quickly saves you money in the long run.

Even if you have to temporarily dip below 20% for this category due to extreme inflationary pressures on your needs, make it a priority to return to and ideally exceed this percentage as soon as possible. The long-term benefits of consistent saving and investing far outweigh short-term sacrifices.

Practical Strategies for Enhanced Personal Budgeting in 2026

Beyond the 50/30/20 rule, several practical strategies can significantly enhance your personal budgeting 2026 efforts. These tips are designed to help you gain better control over your finances and make your money work harder for you.

Automate Your Savings and Bill Payments

One of the most effective ways to stick to any budget is to automate as much as possible. Set up automatic transfers from your checking account to your savings and investment accounts on payday. Similarly, automate bill payments to avoid late fees and ensure your ‘Needs’ are covered consistently. This ‘set it and forget it’ approach removes the temptation to spend money before it reaches your savings goals.

Track Every Dollar

You can’t manage what you don’t measure. Use budgeting apps, spreadsheets, or even a simple notebook to track every dollar you spend. This level of detail helps you identify spending leaks, understand your habits, and make informed adjustments. Many apps can categorize your spending automatically, making this process much easier for personal budgeting 2026.

Conduct Regular Budget Reviews

Your budget isn’t a static document; it’s a living plan. Review it monthly to assess its effectiveness, identify any discrepancies, and make necessary adjustments. Life changes – a new job, a pay raise, unexpected expenses – all require budget modifications. Regular reviews ensure your budget remains relevant and effective in helping you achieve your financial goals.

Build an Emergency Fund (and Replenish It)

An emergency fund is your financial safety net. Aim for at least three to six months’ worth of essential living expenses. In an inflationary environment, the amount needed for your emergency fund will likely increase, so be prepared to adjust your target. This fund prevents you from going into debt when unexpected costs arise, which is crucial for maintaining financial stability in 2026.

Focus on Debt Reduction, Especially High-Interest Debt

High-interest debt, like credit card balances, can quickly spiral out of control, especially if interest rates rise. Make it a priority to pay down these debts aggressively. Consider strategies like the debt snowball or debt avalanche method. Reducing debt frees up more of your income for savings and investments, significantly improving your financial outlook for personal budgeting 2026.

Investing for Growth: Counteracting Inflation’s Bite

Simply saving money in a low-interest savings account during high inflation is akin to watching its value diminish. To truly protect and grow your wealth in 2026, strategic investing is essential. Your personal budgeting 2026 plan must include a robust investment component.

Diversify Your Investment Portfolio

Diversification is key to mitigating risk and maximizing returns. Don’t put all your eggs in one basket. Consider a mix of:

- Stocks: Focus on companies with strong fundamentals, pricing power, and consistent earnings, as they are better positioned to weather inflationary pressures.

- Bonds: While traditional bonds may suffer during inflation, consider inflation-protected securities (TIPS) which are designed to adjust with inflation.

- Real Estate: Historically, real estate has served as a good hedge against inflation, as property values and rental income tend to rise with the cost of living.

- Commodities: Gold, silver, and other commodities can sometimes perform well during inflationary periods.

- Cryptocurrencies: While volatile, some investors see certain cryptocurrencies as a potential hedge against traditional currency inflation, though this comes with higher risk.

Consult with a financial advisor to create a diversified portfolio that aligns with your risk tolerance and financial goals for personal budgeting 2026.

Consider Inflation-Adjusted Investments

Beyond TIPS, explore other financial products designed to offer protection against inflation. These might include certain types of annuities or funds that specifically invest in inflation-sensitive assets. Staying informed about new financial instruments and strategies is crucial.

Rebalance Your Portfolio Regularly

Market conditions change, and so should your portfolio. Regularly review and rebalance your investments to ensure they still align with your financial goals and risk tolerance. This is especially important in a dynamic economic environment like 2026, where inflation can quickly shift the relative performance of different asset classes.

Leveraging Technology for Smarter Budgeting

The digital age offers a plethora of tools to make personal budgeting 2026 easier and more efficient. Embrace technology to streamline your financial management process.

Budgeting Apps and Software

Numerous apps like Mint, YNAB (You Need A Budget), Personal Capital, and PocketGuard can connect to your bank accounts and credit cards, automatically categorize transactions, and provide real-time insights into your spending. These tools can help you visualize your adherence to the 50/30/20 rule and identify areas for improvement.

Financial Planning Tools

Beyond daily budgeting, consider using financial planning software to model different financial scenarios, project your net worth, and plan for long-term goals like retirement or a child’s education. These tools are invaluable for comprehensive personal budgeting 2026.

Online Banking Features

Most modern banks offer robust online and mobile banking platforms that allow you to set up alerts for low balances, track spending, and manage automatic transfers. Utilize these features to stay on top of your finances without constant manual effort.

The Psychological Aspect of Budgeting: Staying Motivated

Budgeting isn’t just about numbers; it’s also about behavior and discipline. Staying motivated, especially when inflation makes things tougher, is critical for successful personal budgeting 2026.

Set Realistic Goals

Don’t set yourself up for failure with overly ambitious goals. Start with small, achievable steps and gradually increase your targets. Celebrating small victories along the way can help maintain motivation.

Find an Accountability Partner

Share your financial goals with a trusted friend, family member, or even a financial coach. Having someone to discuss your progress with and who can hold you accountable can be a powerful motivator.

Educate Yourself Continuously

The more you learn about personal finance, investing, and economics, the more confident and empowered you’ll feel. Read books, listen to podcasts, and follow reputable financial news sources. Knowledge is power when it comes to personal budgeting 2026.

Be Kind to Yourself

There will be times when you deviate from your budget. Don’t let a single setback derail your entire plan. Acknowledge it, learn from it, and get back on track. Consistency over perfection is the key to long-term financial success.

Conclusion: Your Path to Financial Stability in 2026

The economic landscape of 2026, characterized by ongoing inflationary pressures, demands a proactive and adaptable approach to personal budgeting 2026. The 50/30/20 rule provides an excellent foundation, but its application must be nimble and responsive to changing financial realities. By meticulously categorizing your expenses, strategically managing your ‘Wants,’ and diligently prioritizing ‘Savings and Debt Repayment,’ you can build a robust financial plan.

Remember that effective budgeting extends beyond mere allocation; it involves continuous tracking, regular reviews, smart investing to counteract inflation, and leveraging technology to your advantage. Most importantly, it requires a resilient mindset and a commitment to your long-term financial well-being. By embracing these principles, you are not just budgeting; you are actively shaping a future of financial security and freedom.

Start today. Take control of your finances, adapt to the challenges of 2026, and empower yourself to achieve lasting financial stability. Your future self will thank you.