Personal Bankruptcy 2026: A Guide to Financial Recovery

Anúncios

In an ever-evolving economic landscape, understanding your options when facing overwhelming debt is paramount. For many, the concept of personal bankruptcy 2026 might seem daunting, a last resort shrouded in misunderstanding and fear. However, it can be a vital tool for financial recovery, offering a fresh start when other avenues have been exhausted. This comprehensive guide aims to demystify personal bankruptcy in 2026, providing clear insights into its various forms, the filing process, potential impacts, and strategies for rebuilding your financial life.

The decision to file for bankruptcy is rarely an easy one. It often comes after months, or even years, of struggling with debt, dealing with creditor calls, and experiencing significant stress. Our goal here is not to advocate for bankruptcy as a first choice, but to provide accurate, up-to-date information for those who may be considering it, or simply want to understand their options for financial recovery in 2026. We will explore the nuances of Chapter 7 and Chapter 13 bankruptcy, discuss eligibility requirements, and outline what to expect during and after the process. By the end of this article, you should have a clearer picture of whether personal bankruptcy 2026 is the right path for your unique financial situation.

Anúncios

Understanding Personal Bankruptcy 2026: What It Means for You

Personal bankruptcy is a legal process designed to help individuals and businesses who cannot pay their debts. It provides a way for debtors to either eliminate most of their debts or to repay them over time under court supervision. The laws governing bankruptcy are federal, meaning they are the same across all U.S. states, though local court rules and interpretations can vary. When we talk about personal bankruptcy 2026, we’re referring to the current legal framework and economic conditions that will influence bankruptcy filings in the coming year.

The primary purpose of bankruptcy is two-fold: to give an honest debtor a fresh start and to ensure that creditors receive some repayment in an equitable manner. While the idea of wiping out debt can sound appealing, it comes with significant consequences that must be carefully considered. It affects your credit score, your ability to obtain future credit, and can even impact certain types of employment. However, for many, the relief from overwhelming debt and creditor harassment outweighs these drawbacks, paving the way for a healthier financial future. The key is to understand the different types of bankruptcy and which one might align best with your circumstances.

Anúncios

The Two Main Types of Personal Bankruptcy: Chapter 7 vs. Chapter 13

When considering personal bankruptcy 2026, the vast majority of individuals will fall under one of two chapters of the U.S. Bankruptcy Code: Chapter 7 or Chapter 13. Each has distinct characteristics, eligibility requirements, and outcomes.

Chapter 7 Bankruptcy: The Liquidation Option

Chapter 7 bankruptcy, often referred to as ‘liquidation bankruptcy,’ is designed for individuals with limited income who cannot afford to repay their debts. In a Chapter 7 case, a bankruptcy trustee is appointed to oversee the debtor’s assets. The trustee’s role is to sell any non-exempt assets to pay off creditors. However, most Chapter 7 cases for individuals are ‘no-asset’ cases, meaning the debtor’s property is primarily composed of exempt assets, and thus, there is nothing for the trustee to liquidate.

To qualify for Chapter 7, you must pass the ‘means test.’ This test evaluates your income against the median income for your state. If your income is below the median, you generally qualify. If it’s above, further calculations involving your expenses are performed to determine if you have sufficient disposable income to repay your debts. If you fail the means test, you may be directed to file Chapter 13 instead. The primary benefit of Chapter 7 is a relatively quick discharge of most unsecured debts, such as credit card debt, medical bills, and personal loans, usually within 3-6 months.

However, Chapter 7 does not discharge all types of debt. Non-dischargeable debts typically include most student loans, recent tax debts, child support, alimony, and debts incurred through fraud. It also doesn’t allow you to keep property that is not exempt, meaning you could lose valuable assets if they are not protected by state or federal exemptions. Understanding these nuances is crucial when evaluating personal bankruptcy 2026 options.

Chapter 13 Bankruptcy: The Reorganization Option

Chapter 13 bankruptcy, known as ‘reorganization bankruptcy,’ is designed for individuals with regular income who can afford to repay some or all of their debts over time. Unlike Chapter 7, debtors in Chapter 13 propose a repayment plan, typically lasting three to five years, during which they make regular payments to a bankruptcy trustee. The trustee then distributes these payments to creditors according to the approved plan.

Chapter 13 is often chosen by debtors who have valuable assets they wish to protect, such as a home or a car, that might otherwise be liquidated in a Chapter 7 filing. It also allows debtors to catch up on missed mortgage payments and potentially strip off second mortgages or reduce the principal balance on certain car loans. To qualify for Chapter 13, you must have a stable income and your unsecured and secured debts must not exceed certain limits, which are adjusted periodically. The main advantage of Chapter 13 is the ability to keep your property while repaying your debts in a structured, manageable way. Upon successful completion of the repayment plan, remaining dischargeable debts are eliminated.

The downside is the longer commitment and the stricter budgeting required during the repayment period. However, for those with higher incomes or significant assets, Chapter 13 can be a powerful tool for financial recovery, providing a roadmap out of debt without sacrificing everything they own. Both Chapter 7 and Chapter 13 will be prominent options for personal bankruptcy 2026 filers, each serving different financial situations.

Eligibility for Personal Bankruptcy 2026

Not everyone can file for bankruptcy. There are specific eligibility requirements that must be met, which can vary slightly between Chapter 7 and Chapter 13. These requirements are in place to ensure that bankruptcy is used appropriately and to prevent abuse of the system.

Chapter 7 Eligibility: The Means Test and Other Factors

As mentioned, the ‘means test’ is the primary hurdle for Chapter 7 eligibility. It’s a two-part test: first, comparing your current monthly income to the median income of your state for a household of your size. If your income is below the median, you pass. If it’s above, further calculations involving your expenses are performed to determine if you have sufficient disposable income to repay your debts. If you fail the means test, you may be directed to file Chapter 13 instead. The primary benefit of Chapter 7 is a relatively quick discharge of most unsecured debts, such as credit card debt, medical bills, and personal loans, usually within 3-6 months.

Other factors for Chapter 7 eligibility include:

- Prior Filings: You cannot receive a Chapter 7 discharge if you received a Chapter 7 discharge in the past eight years or a Chapter 13 discharge in the past six years.

- Credit Counseling: You must complete a credit counseling course from an approved agency within 180 days before filing for bankruptcy.

- Honesty: You must be an ‘honest debtor,’ meaning you haven’t fraudulently transferred assets or concealed information from the court.

Chapter 13 Eligibility: Income and Debt Limits

Chapter 13 eligibility focuses on your ability to make regular payments and the total amount of your debt. You must have a stable and regular income to propose and complete a repayment plan. There are also debt limits that are adjusted periodically. For personal bankruptcy 2026, these limits will be in effect:

- Secured Debt Limit: Your secured debts (like mortgages or car loans) must not exceed a certain amount.

- Unsecured Debt Limit: Your unsecured debts (like credit cards or medical bills) must also not exceed a certain amount.

- Prior Filings: You cannot receive a Chapter 13 discharge if you received a Chapter 7 discharge in the past four years or a Chapter 13 discharge in the past two years.

- Credit Counseling: Similar to Chapter 7, you must complete an approved credit counseling course.

It’s crucial to consult with a qualified bankruptcy attorney to determine your eligibility, as these rules can be complex and specific to your financial situation. They can help you navigate the requirements for personal bankruptcy 2026.

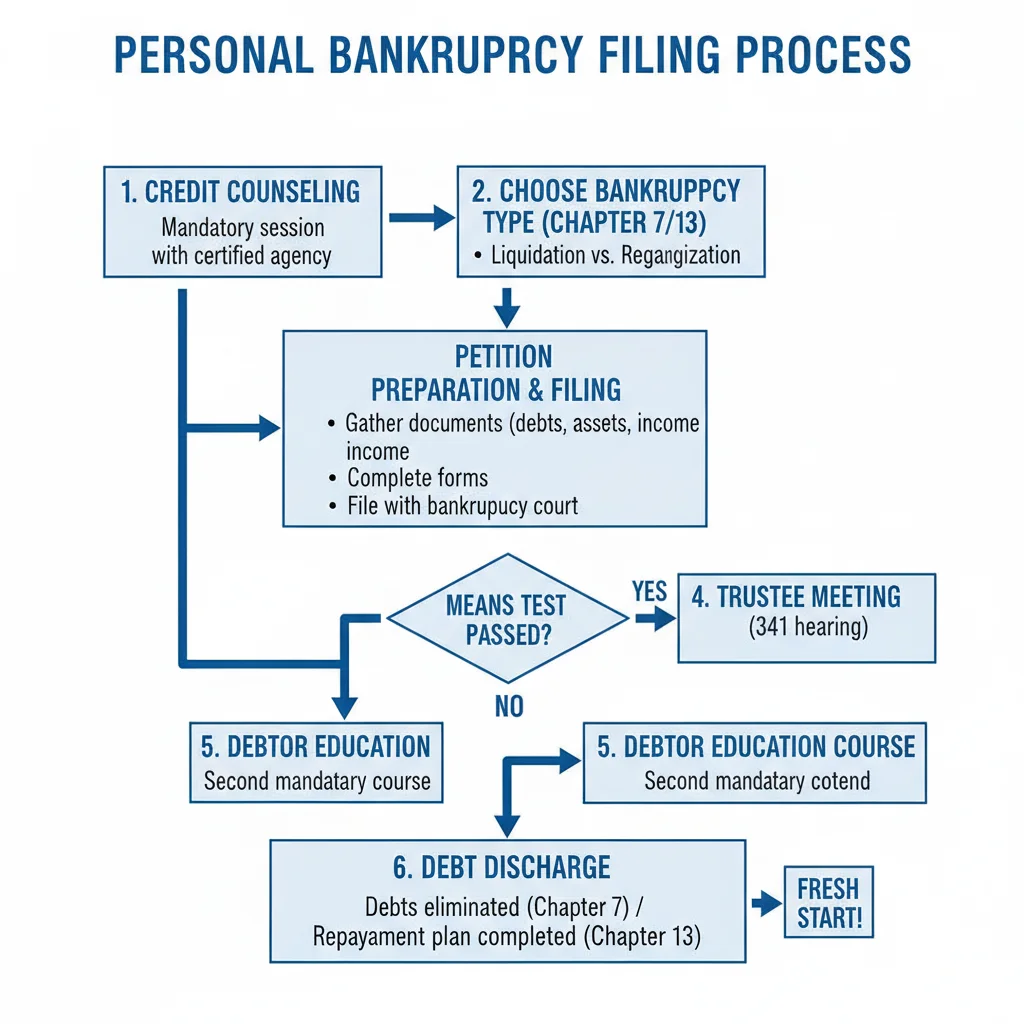

The Personal Bankruptcy 2026 Filing Process: Step-by-Step

Filing for bankruptcy is a legal process that involves several distinct steps. While the specifics can vary slightly depending on the chapter, the general outline remains consistent. Understanding this process can help alleviate some of the anxiety associated with filing for personal bankruptcy 2026.

Step 1: Credit Counseling

Before you can file for either Chapter 7 or Chapter 13, you are required to complete a credit counseling course from a government-approved agency. This course typically lasts about an hour or two and aims to help you explore alternatives to bankruptcy and understand the implications of filing. You must complete this within 180 days before filing your petition.

Step 2: Gathering Documents and Preparing the Petition

This is arguably the most time-consuming step. You’ll need to gather a vast array of financial documents, including:

- Tax returns for the past several years.

- Pay stubs or other proof of income.

- Bank statements.

- Credit reports.

- Statements from all creditors (credit cards, loans, mortgages, etc.).

- Records of any property owned (deeds, titles).

- Monthly living expenses.

With these documents, you or your attorney will prepare the bankruptcy petition and schedules. These are extensive forms that detail your assets, liabilities, income, expenses, and financial history. Accuracy is critical, as providing false information can lead to severe penalties.

Step 3: Filing the Petition

Once the petition and schedules are complete, they are filed with the bankruptcy court in your district. At this point, the ‘automatic stay’ goes into effect. This is a powerful injunction that immediately stops most collection activities, including lawsuits, wage garnishments, repossessions, and foreclosure proceedings. This provides immediate relief from creditor harassment, a significant benefit of personal bankruptcy 2026.

Step 4: Meeting of Creditors (341 Meeting)

Approximately 20 to 40 days after filing, you will attend a ‘meeting of creditors,’ also known as a 341 meeting. Despite the name, creditors rarely attend. This meeting is primarily between you, your attorney (if you have one), and the bankruptcy trustee. The trustee will ask you questions under oath about your petition, assets, debts, and financial affairs to ensure all information is accurate and complete. This is a relatively brief but important part of the personal bankruptcy 2026 process.

Step 5: Debtor Education Course

After filing but before your debts can be discharged, you must complete a second mandatory course: a debtor education course (also known as a financial management course). This course focuses on personal finance, budgeting, and financial planning to help you avoid future financial difficulties. Like the credit counseling course, it must be from an approved provider.

Step 6: Trustee Actions and Discharge

For Chapter 7:

After the 341 meeting, the trustee will review your assets. If there are non-exempt assets, they will be liquidated to pay creditors. If it’s a no-asset case, the trustee will typically file a ‘no distribution’ report. Assuming all requirements are met, the court will issue a discharge order, typically 60-90 days after the 341 meeting. This order legally releases you from personal liability for most of your dischargeable debts.

For Chapter 13:

After the 341 meeting, your proposed repayment plan will be reviewed by creditors and the trustee. If there are objections, you may need to modify the plan. Once approved by the court, you will begin making regular payments to the trustee for the duration of your plan (3-5 years). Upon successful completion of all payments, the court will grant a discharge of your remaining dischargeable debts. This longer process is a key difference in personal bankruptcy 2026 under Chapter 13.

Impacts and Consequences of Personal Bankruptcy 2026

While bankruptcy offers a fresh start, it’s essential to understand its long-term impacts. These consequences, while significant, are often manageable and temporary, especially with proactive planning for financial recovery.

Credit Score and Future Credit

One of the most immediate and well-known impacts of personal bankruptcy is on your credit score. A bankruptcy filing will remain on your credit report for 7 to 10 years (Chapter 13 for 7 years, Chapter 7 for 10 years). This will significantly lower your credit score initially, making it more challenging to obtain new credit, loans, or mortgages at favorable rates. Lenders will view you as a higher risk.

However, it’s important to remember that credit scores are dynamic. With responsible financial habits post-bankruptcy, you can begin to rebuild your credit. Many individuals find that within 2-3 years, they can obtain new credit cards (often secured cards initially) and even car loans, albeit with higher interest rates. The key is consistent, on-time payments and avoiding new debt. This aspect of personal bankruptcy 2026 requires patience and discipline.

Assets and Property

The impact on your assets depends heavily on the type of bankruptcy filed:

- Chapter 7: Non-exempt assets can be sold by the trustee. However, state and federal exemption laws protect a significant amount of property, including equity in a home, a car, household goods, and retirement accounts. Most Chapter 7 filers lose little to no property.

- Chapter 13: You typically keep all your assets, as long as you can make the required payments under your repayment plan. This is a major advantage for homeowners or those with significant equity.

Consulting with an attorney is vital to understand how your specific assets would be treated under personal bankruptcy 2026 laws.

Employment and Housing

Legally, employers cannot discriminate against you solely because you have filed for bankruptcy. However, certain professions, especially those requiring security clearances or financial trustworthiness (e.g., banking, law enforcement), might conduct background checks that reveal a bankruptcy. While it shouldn’t be the sole reason for denial, it could be a factor in some cases.

Finding rental housing post-bankruptcy can sometimes be challenging, as landlords often check credit reports. However, many landlords understand that bankruptcy is a fresh start and will consider other factors, such as stable income and positive references. It might require more effort to find suitable housing, but it’s certainly not impossible.

Psychological and Emotional Impact

Beyond the financial and legal ramifications, filing for bankruptcy can have a significant psychological and emotional impact. Feelings of shame, failure, and anxiety are common. However, many individuals also report a profound sense of relief once the process is underway and the burden of debt is lifted. It’s crucial to acknowledge these feelings and seek support if needed, understanding that bankruptcy is a legal solution designed to help, not punish, those in financial distress. The emotional journey through personal bankruptcy 2026 is as important as the financial one.

Rebuilding Your Financial Future After Personal Bankruptcy 2026

Bankruptcy is not an end but a new beginning. The period following your discharge is critical for establishing healthy financial habits and rebuilding your credit. This phase of financial recovery requires discipline, education, and strategic planning.

1. Establish a Realistic Budget

The first and most important step is to create and stick to a realistic budget. This involves tracking your income and expenses meticulously. Identify areas where you can cut back and prioritize essential spending. A budget is your roadmap to financial stability and prevents you from falling back into debt. The debtor education course you completed should provide a solid foundation for this.

2. Save for Emergencies

One of the primary reasons many people fall into debt is a lack of emergency savings. Aim to build an emergency fund that can cover 3-6 months of essential living expenses. Start small, even if it’s just $50 a month. Having this safety net will prevent you from relying on credit cards when unexpected expenses arise, a crucial lesson from navigating personal bankruptcy 2026.

3. Rebuild Your Credit Strategically

Rebuilding credit takes time, but it’s achievable. Here’s how:

- Secured Credit Cards: These cards require a cash deposit, which acts as your credit limit. They report to credit bureaus and can help you demonstrate responsible credit usage.

- Small Installment Loans: A small, short-term loan that you repay on time can also help. Ensure the lender reports to all three major credit bureaus.

- Authorized User: If a trusted family member has excellent credit, becoming an authorized user on their credit card can sometimes boost your score, provided they use it responsibly.

- Monitor Your Credit: Regularly check your credit report for errors and monitor your score’s progress.

4. Avoid New Debt

This might seem obvious, but it’s easy to fall back into old habits. Be extremely cautious about taking on new debt, especially high-interest credit cards. If you do get new credit, use it sparingly and pay off the balance in full each month. The goal is to build a positive payment history, not accumulate new debt.

5. Continue Your Financial Education

Financial literacy is an ongoing journey. Read books, attend workshops, and utilize online resources to continuously improve your understanding of personal finance. The more knowledgeable you are, the better equipped you’ll be to make sound financial decisions and avoid future pitfalls. This continuous learning is vital for long-term financial recovery after personal bankruptcy 2026.

6. Seek Professional Guidance

Consider working with a financial advisor or credit counselor after bankruptcy. They can help you create a personalized financial plan, set achievable goals, and provide ongoing support as you navigate your new financial landscape. Their expertise can be invaluable in accelerating your financial recovery.

Alternatives to Personal Bankruptcy

Before considering personal bankruptcy 2026, it’s wise to explore other debt relief options. Bankruptcy should always be a last resort, as other solutions may be less impactful on your credit and offer a viable path to debt resolution.

Debt Management Plans (DMPs)

Offered by non-profit credit counseling agencies, DMPs involve working with counselors who negotiate with your creditors to lower interest rates, waive fees, and set up a single, manageable monthly payment. While DMPs don’t reduce the principal amount of debt, they can make repayment more affordable and help you become debt-free in 3-5 years. They have a less severe impact on your credit than bankruptcy.

Debt Consolidation Loans

A debt consolidation loan involves taking out a new loan to pay off multiple existing debts. Ideally, the new loan has a lower interest rate and a single monthly payment, simplifying your finances and potentially saving you money. However, you need a decent credit score to qualify for favorable terms, and if you continue to use credit cards, you could end up in more debt.

Debt Settlement

Debt settlement involves negotiating with creditors to pay a lump sum that is less than the total amount owed. This can be effective, but it comes with risks. It can negatively impact your credit score, and creditors are not obligated to negotiate. Furthermore, settled debt may be considered taxable income by the IRS. It’s a more aggressive approach than DMPs and should be approached with caution.

Doing Nothing

While not a recommended strategy, some people choose to do nothing, hoping their financial situation will improve. This often leads to increased debt, higher interest, more fees, and aggressive collection efforts, including lawsuits and wage garnishments. Ignoring debt is never a viable long-term solution.

Evaluating these alternatives alongside personal bankruptcy 2026 is a critical step in making an informed decision about your financial future. An attorney or credit counselor can help you assess which option is best for your specific circumstances.

Conclusion: A New Beginning with Personal Bankruptcy 2026

Facing overwhelming debt is an incredibly stressful experience, but it’s a challenge that many individuals overcome through strategic financial planning and, when necessary, legal avenues like personal bankruptcy. Understanding personal bankruptcy 2026 means recognizing it not as a failure, but as a structured legal process designed to provide a much-needed fresh start. Whether it’s Chapter 7 for a quick discharge of unsecured debts or Chapter 13 for a managed repayment plan, bankruptcy offers a path out of seemingly insurmountable financial distress.

The journey through bankruptcy is complex, involving strict eligibility requirements, meticulous documentation, and several court appearances. However, the immediate relief from creditor harassment provided by the automatic stay, coupled with the eventual discharge of debts, can significantly reduce stress and pave the way for a more stable financial future. While there are undeniable impacts on credit and future financial opportunities, these are often temporary and manageable with diligent effort towards financial recovery.

The most crucial takeaway is that bankruptcy is a tool, and like any tool, its effectiveness depends on how it’s used. It requires honesty, commitment to financial education, and a willingness to implement new, healthier spending and saving habits. Rebuilding credit, establishing an emergency fund, and living within a budget are not just post-bankruptcy tasks; they are foundational principles for long-term financial health. Before making any decisions, always seek advice from a qualified bankruptcy attorney or an accredited credit counselor. They can provide personalized guidance, clarify the intricacies of personal bankruptcy 2026 laws, and help you determine the best course of action for your unique situation. With careful planning and perseverance, a brighter financial future is within reach, even after navigating the challenges of bankruptcy.