Gift Tax Exclusions 2026: Optimize Your Wealth Transfer Strategy

Anúncios

Gift Tax Exclusions 2026: Optimize Your Wealth Transfer Strategy

Understanding the nuances of Gift Tax Exclusions is paramount for anyone looking to transfer wealth efficiently and effectively. As we approach 2026, it’s crucial to be well-informed about the updated limits and rules that will govern your philanthropic endeavors or intergenerational wealth transfers. This comprehensive guide will delve into the intricacies of Gift Tax Exclusions for 2026, providing you with the knowledge to make informed decisions and optimize your financial planning.

The act of giving, whether to family, friends, or charitable organizations, is often driven by genuine affection and a desire to support loved ones or causes. However, without proper planning, these generous acts can inadvertently trigger gift tax implications. The Internal Revenue Service (IRS) imposes a gift tax on transfers of property by gift, but it also provides specific exclusions and exemptions to mitigate this tax burden. Navigating these rules correctly can save you and your recipients significant amounts of money and ensure your wealth transfer goals are met without unnecessary complications.

Anúncios

This article will cover the fundamental concepts of gift tax, explain the annual Gift Tax Exclusions, discuss the lifetime gift tax exemption, and explore various strategies for maximizing your giving potential in 2026. We will also touch upon the potential changes and economic factors that might influence these limits, offering a forward-looking perspective on estate planning.

What is Gift Tax? A Fundamental Understanding

Before diving into the specifics of Gift Tax Exclusions for 2026, it’s essential to grasp the basic definition of gift tax. In the United States, gift tax is a federal tax on the transfer of property from one individual to another while receiving nothing, or less than full value, in return. The gift tax applies whether the donor intends the transfer to be a gift or not. The primary responsibility for paying the gift tax generally falls on the donor, not the recipient.

Anúncios

The purpose of the gift tax, alongside the estate tax, is to prevent individuals from avoiding estate taxes by simply giving away all their assets before death. The two taxes are unified, meaning that gifts made during your lifetime reduce the amount of your unified credit that can be used to offset estate taxes after your death. This unified system ensures a consistent approach to taxing wealth transfers, regardless of when they occur.

It’s important to note that not all transfers are considered taxable gifts. For instance, transfers to political organizations, payments for tuition or medical expenses made directly to the institution, and gifts to your spouse (if they are a U.S. citizen) are generally exempt from gift tax. These specific exemptions provide additional avenues for tax-free wealth transfer, independent of the annual Gift Tax Exclusions.

Understanding these foundational principles is the first step toward developing a robust wealth transfer strategy. As we move closer to 2026, staying informed about any legislative changes that might impact these definitions or exemptions will be critical for effective financial planning.

The Annual Gift Tax Exclusion: Your Key to Tax-Free Giving

The annual Gift Tax Exclusion is arguably the most powerful tool in your wealth transfer arsenal. It allows you to give away a certain amount of money or property to any number of individuals each year without incurring gift tax and without using up any of your lifetime gift tax exemption. This exclusion is per donor, per recipient, per year.

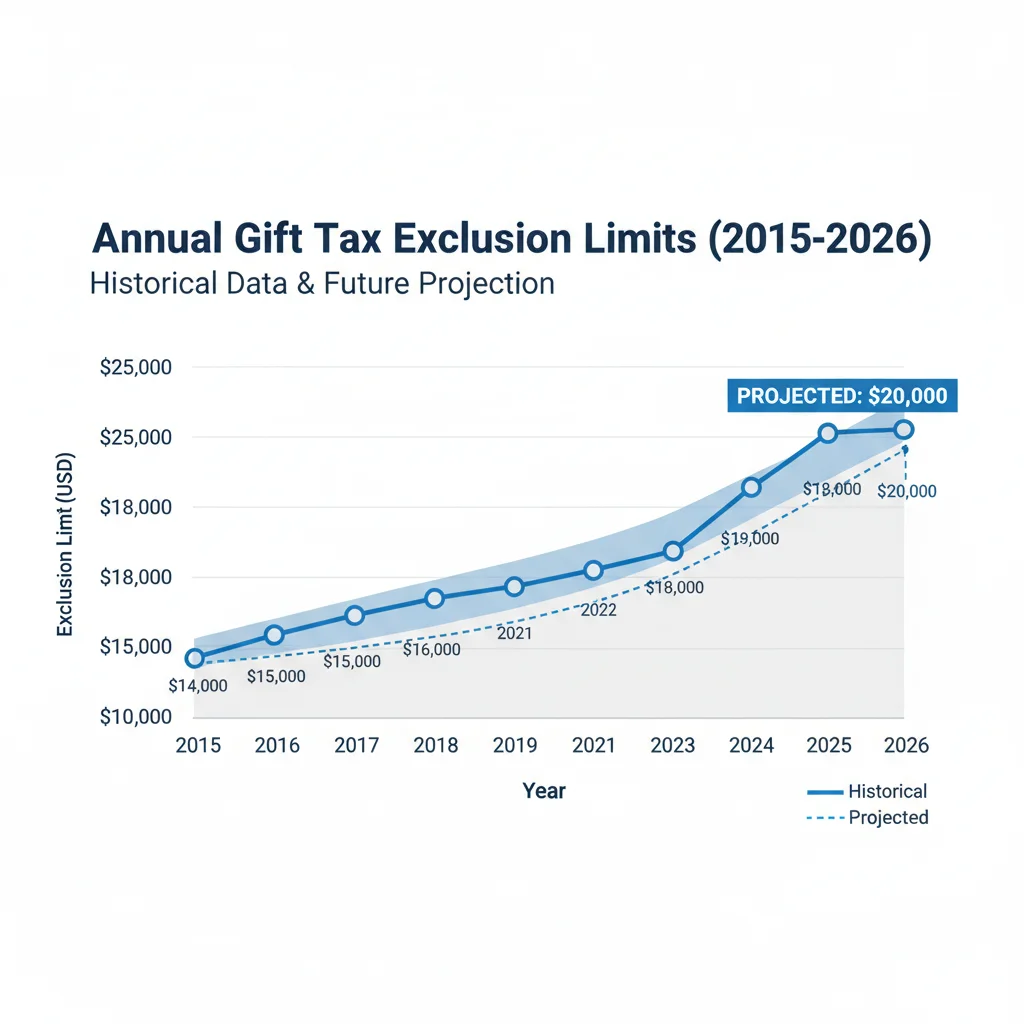

Projected Annual Exclusion for 2026

While the official figure for 2026 Gift Tax Exclusions is typically announced by the IRS in late 2025, based on historical inflation adjustments, we can anticipate a slight increase from previous years. For reference, the annual exclusion for 2024 was $18,000 per donee. Assuming a consistent inflation rate, the 2026 exclusion could be around $19,000 or even $20,000 per donee. It is crucial to monitor IRS announcements for the definitive figure as it becomes available.

This exclusion is not cumulative. If you don’t use your full annual exclusion in one year, you cannot carry it over to the next. Therefore, a proactive approach to gifting each year can be highly beneficial for maximizing tax-free transfers over time.

How the Annual Exclusion Works in Practice

Let’s illustrate with an example: If the 2026 annual Gift Tax Exclusion is $19,000, you and your spouse could each give $19,000 to your child, for a total of $38,000, without any gift tax implications or using any of your lifetime exemption. If you have three children, you and your spouse could collectively give them $114,000 ($38,000 x 3) in 2026, completely tax-free and without filing a gift tax return (Form 709) for these gifts.

This strategy is particularly effective for families with multiple donees and for those who wish to slowly reduce the size of their taxable estate over many years. By consistently utilizing the annual exclusion, you can transfer substantial wealth without ever touching your lifetime exemption or incurring gift tax.

The Lifetime Gift Tax Exemption and Its Role in 2026

Beyond the annual Gift Tax Exclusions, you also have a lifetime gift tax exemption. This exemption represents the total amount of money or property you can give away during your lifetime (above the annual exclusion amount) or leave at your death without incurring federal gift or estate tax. This is often referred to as the unified credit, as it applies to both gifts made during life and assets left at death.

Current and Projected Lifetime Exemption

The lifetime gift and estate tax exemption has seen significant fluctuations in recent years. Under the Tax Cuts and Jobs Act (TCJA) of 2017, the exemption amount was substantially increased. For 2024, it stands at $13.61 million per individual. However, a critical point for 2026 planning is that many provisions of the TCJA are set to expire at the end of 2025. This means that, without new legislation, the lifetime exemption amount is scheduled to revert to approximately $7 million per individual (adjusted for inflation) in 2026.

This anticipated reduction in the lifetime exemption makes understanding and strategically utilizing Gift Tax Exclusions and the current higher lifetime exemption even more urgent for high-net-worth individuals. If you have a large estate, making significant gifts before the end of 2025 could allow you to take advantage of the higher exemption amount, provided you consult with a qualified estate planning attorney or financial advisor.

Using the Lifetime Exemption Wisely

Gifts that exceed the annual exclusion amount will begin to chip away at your lifetime exemption. For example, if the annual exclusion is $19,000 in 2026 and you give a single individual $50,000, $19,000 of that gift is covered by the annual exclusion, and the remaining $31,000 will reduce your lifetime exemption. You would also need to file a Form 709, U.S. Gift (and Generation-Skipping Transfer) Tax Return, to report this gift.

For married couples, there is also the concept of ‘gift splitting.’ If both spouses agree, they can elect to split gifts made by one spouse to a third party. This effectively doubles the annual exclusion amount available for a single gift from one spouse, even if only one spouse actually made the gift, without using the other spouse’s annual exclusion on other gifts. This strategy requires both spouses to consent and file a joint gift tax return.

Strategic Planning with Gift Tax Exclusions for 2026

Effective wealth transfer goes beyond simply knowing the limits; it involves strategic planning to maximize the benefits of Gift Tax Exclusions and the lifetime exemption. Here are several strategies to consider as you plan for 2026:

1. Maximize Annual Exclusions Annually

The most straightforward strategy is to consistently utilize the annual exclusion for gifts to as many recipients as you desire. This can include children, grandchildren, nieces, nephews, and even close friends. By making these gifts each year, you can significantly reduce your taxable estate over time without incurring any gift tax liability or using your lifetime exemption.

2. Consider ‘Crummey’ Trusts for Minors

Gifts to minors often present a challenge because, to qualify for the annual Gift Tax Exclusions, the gift must be a ‘present interest’ – meaning the recipient must have an immediate right to use or enjoy the gifted property. A ‘Crummey’ trust is an irrevocable trust designed to hold assets for minors while allowing gifts to the trust to qualify for the annual exclusion. The trust beneficiaries are given a temporary right to withdraw gifted funds (the ‘Crummey power’), which makes the gift a present interest. This power typically lapses after a short period, allowing the funds to remain in the trust for the minor’s future benefit.

3. Direct Payment of Tuition and Medical Expenses

As mentioned earlier, payments made directly to an educational institution for tuition or to a medical provider for medical care are not considered taxable gifts, regardless of the amount. This is a powerful exclusion that operates independently of the annual Gift Tax Exclusions and the lifetime exemption. If you wish to help a loved one with these significant expenses, paying the institution directly can be a highly tax-efficient way to do so.

4. Spousal Gifting and Gift Splitting

For married couples, the unlimited marital deduction allows for tax-free transfers between spouses who are U.S. citizens. This is a fundamental principle of estate planning. Furthermore, gift splitting allows a married couple to combine their individual annual exclusions, effectively doubling the amount they can give to any single individual each year without gift tax implications. This requires filing a gift tax return (Form 709) to elect gift splitting, even if no tax is due.

5. Utilizing the Higher Lifetime Exemption Before 2026

Given the anticipated reduction in the lifetime exemption in 2026, individuals with substantial wealth should seriously consider making large gifts before the end of 2025 to take advantage of the current, higher exemption amount. The IRS has confirmed that there will be no ‘clawback’ of the benefit of the higher exemption if it is used before the reduction. This means that if you make a gift that uses part of the higher exemption amount before it drops, that gift will not be subject to additional tax later, even if your remaining exemption is lower.

This strategy is complex and requires careful consideration of liquidity, family dynamics, and potential future needs. Consulting with an experienced estate planning attorney and a financial advisor is highly recommended to determine if this is the right strategy for your unique circumstances.

Understanding the Impact of Inflation on Gift Tax Exclusions

The annual Gift Tax Exclusions and the lifetime exemption are typically adjusted for inflation. These adjustments are usually announced by the IRS towards the end of the year for the upcoming calendar year. While these adjustments are often incremental, they reflect the ongoing economic conditions and purchasing power of money.

For 2026, the inflation adjustment will play a role in determining the exact annual exclusion amount, and if the TCJA provisions expire, it will also influence the inflation-adjusted baseline for the reduced lifetime exemption. Keeping an eye on inflation rates and IRS announcements is crucial for accurate planning.

Common Misconceptions About Gift Tax

Despite the clear rules, several misconceptions often lead to confusion regarding gift tax. Clarifying these can help you avoid costly mistakes and plan more effectively around Gift Tax Exclusions.

Misconception 1: All gifts are taxable.

Reality: This is incorrect. As discussed, the annual Gift Tax Exclusions, direct payments for tuition and medical expenses, and gifts to spouses (who are U.S. citizens) or political organizations are all examples of gifts that are not subject to gift tax.

Misconception 2: The recipient pays the gift tax.

Reality: Generally, the donor is responsible for paying the gift tax. In rare circumstances, the recipient may agree to pay the tax, but this must be explicitly arranged and can have its own tax implications.

Misconception 3: You only need to report gifts above the lifetime exemption.

Reality: You must file a gift tax return (Form 709) for any gift to an individual that exceeds the annual exclusion amount, even if no tax is due because of the lifetime exemption. This is how the IRS keeps track of how much of your lifetime exemption you’ve used.

Misconception 4: Loans to family members are gifts.

Reality: A bona fide loan with a reasonable interest rate and a repayment schedule is generally not considered a gift. However, if the loan is interest-free or below market rate, or if there’s no expectation of repayment, the IRS may recharacterize it as a gift, with potential gift tax implications on the forgone interest or the principal amount.

The Role of Professional Advice in Gift Tax Planning

Given the complexities and potential for significant tax implications, seeking professional advice is highly recommended when planning for Gift Tax Exclusions and overall wealth transfer. An experienced estate planning attorney can help you understand the current laws, draft necessary legal documents (like trusts), and ensure your gifting strategy aligns with your overall estate plan.

A qualified financial advisor can help you assess your financial situation, project future needs, and determine the optimal timing and amounts for gifts. They can also assist with the investment and management of assets intended for gifting or held in trusts.

Lastly, a tax professional (such as a CPA) can ensure that all gift tax returns (Form 709) are filed correctly and on time, and they can provide guidance on any state-specific gift or inheritance tax laws that might apply in your jurisdiction. While federal laws primarily govern gift tax, some states have their own estate or inheritance taxes that could impact your planning.

Looking Ahead: Potential Changes Beyond 2026

While our focus is primarily on Gift Tax Exclusions for 2026, it’s important to acknowledge that tax laws are subject to change. The expiration of the TCJA provisions at the end of 2025 is a significant event, but future legislative actions could further modify gift and estate tax rules. Economic conditions, political shifts, and societal priorities can all influence tax policy.

Staying informed through reliable financial news sources and maintaining an ongoing relationship with your financial and legal advisors will be crucial for adapting your wealth transfer strategy to any future changes. Proactive planning, rather than reactive adjustments, is always the most effective approach.

Conclusion: Empowering Your Wealth Transfer with 2026 Gift Tax Exclusions

The ability to transfer wealth to loved ones or charitable causes is a significant aspect of financial freedom and legacy planning. By thoroughly understanding and strategically utilizing the Gift Tax Exclusions for 2026, you can ensure your generosity is both impactful and tax-efficient.

Remember the key takeaways: the annual exclusion provides a powerful tool for regular tax-free gifts, the lifetime exemption offers a substantial buffer for larger transfers (though it’s set to decrease in 2026), and specific exclusions for tuition and medical expenses offer additional avenues for support. Combining these tools with careful planning, potentially involving trusts and gift splitting for married couples, can optimize your wealth transfer strategy.

As 2026 approaches, review your current financial situation, assess your gifting goals, and consult with a team of trusted financial and legal professionals. Their expertise will be invaluable in navigating the complexities of gift tax laws and helping you craft a robust plan that secures your legacy and supports those you care about most. Don’t let misconceptions or a lack of planning diminish the power of your generosity. Embrace the opportunities presented by the 2026 Gift Tax Exclusions to make your wealth transfer goals a reality.

and IRA Contributions")