Understanding Personal Insurance Needs in 2026: Ensuring Adequate Coverage for Life’s Uncertainties

In an ever-evolving world, safeguarding your future and the well-being of your loved ones is paramount. As we navigate the complexities of 2026, the landscape of personal risks and financial vulnerabilities continues to shift. This makes a thorough understanding and regular review of your personal insurance needs not just advisable, but absolutely essential. Insurance isn’t merely a safety net; it’s a proactive strategy to protect against unforeseen events, mitigate financial losses, and provide peace of mind.

The purpose of this comprehensive guide is to empower you with the knowledge needed to assess, secure, and optimize your personal insurance portfolio. We’ll delve into the various types of personal insurance, discuss how to identify your unique risks, and offer actionable insights to ensure that your coverage remains adequate and relevant in the current economic and social climate. From life’s major milestones to unexpected challenges, having the right insurance in place can make all the difference between recovery and prolonged hardship.

Anúncios

The Evolving Landscape of Personal Risks in 2026

The year 2026 brings with it a unique set of challenges and opportunities that directly impact our personal insurance needs. Technological advancements, climate change, economic fluctuations, and shifts in healthcare policies all contribute to a dynamic risk environment. Cyber threats, for instance, are more prevalent than ever, making identity theft protection and cyber liability coverage increasingly important. Similarly, the growing frequency and intensity of natural disasters underscore the need for robust property and casualty insurance.

Moreover, health concerns continue to evolve, with new medical breakthroughs and rising healthcare costs influencing the demand for comprehensive health and long-term care insurance. Economic volatility can affect job security, highlighting the importance of disability and unemployment insurance. Understanding these macro trends is the first step in tailoring your personal insurance strategy to the realities of today and tomorrow.

Anúncios

Key Pillars of Personal Insurance: What You Need to Know

When discussing personal insurance needs, it’s crucial to understand the fundamental types of coverage available. Each serves a distinct purpose in protecting different aspects of your life and assets.

Life Insurance: Protecting Your Legacy

Life insurance is perhaps one of the most critical components of any personal financial plan, especially for those with dependents. It provides a financial payout to your beneficiaries upon your passing, ensuring their financial stability. In 2026, considering factors like inflation, anticipated future expenses, and existing debts, the amount of coverage needed might be higher than you initially think.

- Term Life Insurance: Offers coverage for a specific period (e.g., 10, 20, or 30 years). It’s generally more affordable and suitable for covering specific financial obligations like a mortgage or children’s education during their formative years.

- Whole Life Insurance: Provides lifelong coverage and includes a savings component (cash value) that grows over time. While more expensive, it offers permanence and can be a valuable asset for estate planning.

- Universal Life Insurance: Offers flexibility in premium payments and death benefits, allowing adjustments to suit changing life circumstances.

When assessing your life insurance personal insurance needs, consider your income, debts (mortgage, loans), future financial goals (college tuition, retirement for your spouse), and any special needs your dependents might have.

Health Insurance: Your Shield Against Medical Costs

Access to quality healthcare is a fundamental necessity, and health insurance is your primary defense against the escalating costs of medical treatment. The specifics of health insurance can vary significantly based on your location, employment status, and personal health circumstances.

- Employer-Sponsored Plans: Often the most common and cost-effective option, offering a range of benefits.

- Individual Plans: Purchased directly from insurance providers or through government marketplaces.

- Medicare/Medicaid: Government programs for eligible seniors, low-income individuals, and those with certain disabilities.

In 2026, it’s vital to review your health insurance policy annually to ensure it adequately covers your and your family’s medical personal insurance needs, including prescription drugs, specialist visits, and mental health services. High-deductible health plans (HDHPs) coupled with Health Savings Accounts (HSAs) remain a popular option for those seeking lower premiums and tax-advantaged savings for medical expenses.

Homeowners/Renters Insurance: Protecting Your Dwelling and Possessions

Your home is likely your most significant asset, and your personal belongings represent years of accumulation. Homeowners insurance protects your dwelling, personal property, and offers liability coverage in case someone is injured on your property. Renters insurance, while not covering the structure, protects your personal belongings and provides liability coverage.

Key considerations for your personal insurance needs in this area include:

- Replacement Cost vs. Actual Cash Value: Opt for replacement cost coverage for your belongings to ensure you can replace them with new items without depreciation.

- Flood and Earthquake Insurance: Standard homeowners policies typically exclude these. If you live in a prone area, separate policies are crucial.

- Riders for Valuables: For high-value items like jewelry, art, or collectibles, consider adding specific riders to your policy.

Regularly inventorying your possessions and updating your policy to reflect significant purchases or home improvements is a smart practice.

Auto Insurance: On the Road to Protection

For most adults, auto insurance is a legal requirement and a financial necessity. It protects you against financial losses in the event of an accident, theft, or other damage to your vehicle. The types of coverage typically include:

- Liability Coverage: Covers damages and injuries you cause to others.

- Collision Coverage: Pays for damage to your own vehicle from a collision.

- Comprehensive Coverage: Covers non-collision damage, such as theft, vandalism, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: Protects you if you’re hit by a driver without adequate insurance.

As vehicle technology advances, consider how features like advanced driver-assistance systems (ADAS) might impact your premiums and your specific personal insurance needs. Telematics programs, which monitor driving habits, can also offer discounts for safe drivers.

Disability Insurance: Protecting Your Income

Often overlooked, disability insurance is vital. It replaces a portion of your income if you become unable to work due to illness or injury. Your ability to earn an income is arguably your most valuable asset.

- Short-Term Disability: Typically covers a few weeks to a few months.

- Long-Term Disability: Provides coverage for extended periods, potentially until retirement age.

Evaluate your existing sick leave, savings, and any employer-provided disability benefits to determine the extent of your personal insurance needs for this crucial coverage.

Long-Term Care Insurance: Planning for Future Needs

As life expectancies increase, the potential need for long-term care (nursing home, assisted living, in-home care) becomes a significant financial consideration. Long-term care insurance helps cover these costs, which are generally not fully covered by health insurance or Medicare.

Umbrella Insurance: The Ultimate Safety Net

An umbrella policy provides additional liability coverage beyond what your auto and homeowners policies offer. If a judgment against you exceeds the limits of your primary policies, umbrella insurance kicks in, protecting your assets from significant lawsuits. This is especially important for individuals with substantial assets or those in professions with higher liability risks.

Assessing Your Unique Personal Insurance Needs in 2026

Determining your specific personal insurance needs requires a personalized approach. There’s no one-size-fits-all solution. Here’s a structured way to assess your situation:

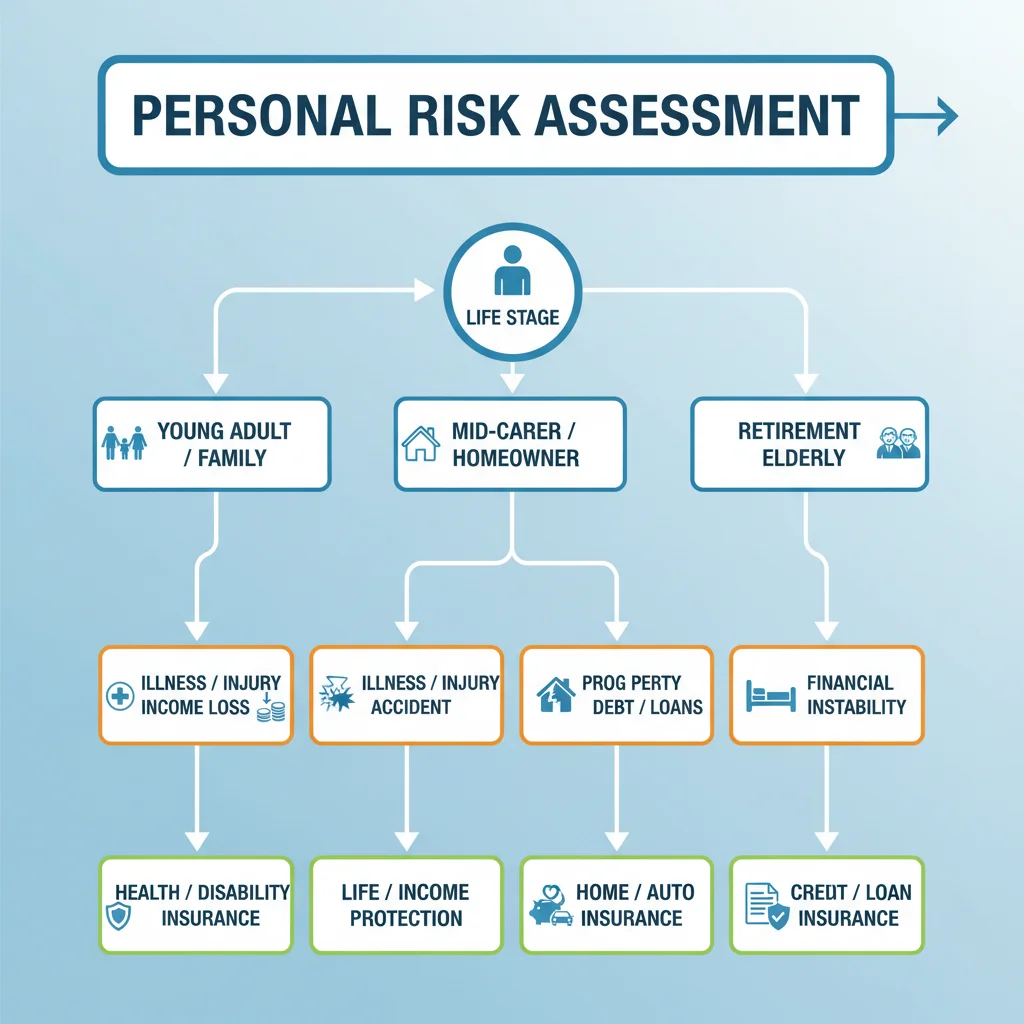

Step 1: Evaluate Your Current Life Stage and Dependents

- Single & Young: Focus on health insurance, auto insurance, and potentially renters insurance. Disability insurance becomes more important as your income grows.

- Married/Partnership: Add life insurance (especially if you have shared debts), review health insurance for family coverage, and consider joint property insurance.

- Parents with Young Children: Life insurance becomes critical, ensuring financial support for your children’s upbringing and education. Increase health insurance coverage.

- Empty Nesters: You might be able to reduce life insurance coverage as financial obligations decrease. Focus shifts to long-term care and retirement planning.

- Retirees: Emphasize Medicare supplements, long-term care, and ensuring your estate plan is solid.

Step 2: Inventory Your Assets and Liabilities

Make a comprehensive list of everything you own (home, cars, savings, investments) and everything you owe (mortgage, student loans, credit card debt). This inventory helps determine the amount of coverage needed to protect your wealth and cover your obligations in various scenarios.

- Assets: Real estate, vehicles, investments, retirement accounts, valuable personal property.

- Liabilities: Mortgage, car loans, student loans, personal loans, credit card debt.

The total value of your assets often dictates the need for higher liability limits, particularly through umbrella insurance, to protect against potential lawsuits.

Step 3: Analyze Your Lifestyle and Risk Factors

Your daily activities and personal choices significantly influence your personal insurance needs:

- Commute: A long daily commute might warrant higher auto insurance limits.

- Dangerous Hobbies: Skydiving, rock climbing, or other high-risk activities can impact life and disability insurance premiums or require specialized coverage.

- Travel: Frequent international travel might necessitate travel insurance or specific health insurance riders.

- Home-Based Business: If you run a business from home, your homeowners policy might not cover business-related liabilities or equipment. You might need a separate business owner’s policy (BOP) or an endorsement.

- Health Conditions: Pre-existing conditions will influence health insurance choices and potentially life and disability insurance.

Step 4: Understand Your Financial Goals and Future Plans

Are you planning to buy a new home, start a family, or retire early? Your long-term financial goals should align with your insurance strategy. For example, if you plan to retire in 10 years, your long-term care insurance needs might become more immediate.

Optimizing Your Insurance Portfolio: Strategies for 2026

Once you’ve assessed your personal insurance needs, the next step is to optimize your coverage. This isn’t just about buying policies; it’s about smart planning, cost-efficiency, and ensuring comprehensive protection.

Regular Reviews and Adjustments

Life is dynamic, and so are your insurance needs. Major life events like marriage, divorce, childbirth, job changes, purchasing a home, or retirement are prime opportunities to review and adjust your policies. Even without significant changes, an annual review is recommended to ensure your coverage remains adequate and competitive.

- Annual Check-up: Schedule a yearly review with your insurance agent or financial advisor.

- Life Event Triggers: Immediately review policies after major life changes.

Bundling Policies for Savings

Many insurance providers offer discounts when you bundle multiple policies (e.g., auto and homeowners). This can lead to significant savings and simplifies managing your policies with a single provider.

Understanding Deductibles and Premiums

A higher deductible typically means lower premiums. While this can save you money upfront, ensure you have sufficient emergency savings to cover the deductible if you need to file a claim. Striking the right balance between affordable premiums and manageable deductibles is key to smart insurance planning.

Leveraging Technology and Digital Tools

In 2026, technology plays a pivotal role in managing personal insurance needs. Online comparison tools, mobile apps from insurance providers, and digital policy management platforms make it easier to compare quotes, understand policy details, and file claims. Utilize these resources to your advantage.

Seeking Professional Advice

Navigating the complexities of insurance can be daunting. A qualified independent insurance agent or financial advisor can provide invaluable guidance. They can help you:

- Identify gaps in your current coverage.

- Compare offerings from various insurers.

- Explain complex policy terms.

- Tailor solutions to your specific personal insurance needs and budget.

Common Pitfalls to Avoid in 2026 Insurance Planning

Even with the best intentions, individuals can make mistakes that compromise their insurance coverage. Be aware of these common pitfalls:

- Underinsurance: Having insufficient coverage to fully protect your assets or meet financial obligations. This is a common issue with homeowners insurance where coverage hasn’t kept pace with rising property values or construction costs.

- Overinsurance: Paying for more coverage than you realistically need, leading to unnecessary expenses. While less risky than underinsurance, it’s still inefficient.

- Ignoring Policy Exclusions: Not reading the fine print can lead to nasty surprises when a claim is denied due to an exclusion you weren’t aware of.

- Failing to Update Beneficiaries: Life events like divorce or remarriage require updating beneficiaries on life insurance policies and retirement accounts.

- Not Shopping Around: Loyalty to one insurer is commendable, but not regularly comparing quotes means you could be missing out on better rates or more suitable coverage options.

- Forgetting About Inflation: The cost of living and replacing assets increases over time. Ensure your coverage amounts are adjusted for inflation.

The Future of Personal Insurance: Trends to Watch

As we look beyond 2026, several trends will continue to shape the personal insurance landscape:

- Personalized Pricing: Data analytics and AI will enable more granular risk assessment, leading to highly personalized premiums based on individual behavior (e.g., telematics for auto insurance, wellness programs for health insurance).

- Embedded Insurance: Insurance options becoming seamlessly integrated into other products and services, like travel insurance offered during flight booking or device protection when purchasing electronics.

- Parametric Insurance: Payouts triggered automatically based on predefined events (e.g., a certain wind speed for hurricane insurance) rather than traditional claims processes.

- Cyber Insurance Expansion: As digital lives become more complex, cyber insurance for individuals will become a standard component of personal insurance needs.

- Climate Change Impact: Insurers will continue to adapt to increasing climate-related risks, potentially leading to higher premiums in vulnerable areas and new types of coverage.

- Digital-First Experiences: The entire insurance journey, from quotes to claims, will become increasingly digital, emphasizing convenience and speed.

Staying informed about these trends will help you anticipate future changes and proactively adjust your personal insurance needs.

Conclusion: Your Proactive Approach to Personal Insurance Needs in 2026

In conclusion, understanding and actively managing your personal insurance needs in 2026 is a cornerstone of robust financial planning. Insurance is not an expense; it’s an investment in your peace of mind and financial resilience. By taking the time to assess your current situation, identify potential risks, and explore the various coverage options available, you empower yourself to make informed decisions that safeguard your future.

Remember, life is a journey filled with both expected joys and unforeseen challenges. With a well-thought-out personal insurance strategy, you can face these uncertainties with confidence, knowing that you and your loved ones are adequately protected. Don’t wait for a crisis to realize the importance of proper coverage. Start your comprehensive insurance review today, consult with professionals, and build a protective shield around your life and assets for 2026 and beyond.