Personal Mortgage Rates 2026: Refinancing Insights for Homeowners

Anúncios

As we navigate the ever-evolving financial landscape, understanding the trajectory of personal mortgage rates in 2026 is paramount for homeowners. Whether you’re contemplating a refinance, planning a home equity loan, or simply want to stay informed about your largest financial commitment, the current and projected state of mortgage rates profoundly impacts your financial well-being. The year 2026, while still a glimpse into the future, is not too far off for strategic planning. Economic indicators, central bank policies, and global events all play a crucial role in shaping these rates, making it essential for homeowners to be well-versed in the factors at play.

The housing market has seen unprecedented shifts in recent years, from record-low interest rates that spurred a refinancing boom to subsequent increases that have tempered buyer enthusiasm. What does this mean for homeowners looking ahead to 2026? This comprehensive guide will delve into expert predictions, analyze key economic drivers, and provide actionable insights for those considering refinancing or making other significant mortgage-related decisions in the coming years. Our focus is to equip you with the knowledge to make informed choices, ensuring your financial strategy aligns with the expected market conditions for Mortgage Rates 2026.

Anúncios

Understanding the Current Mortgage Rate Environment Leading to 2026

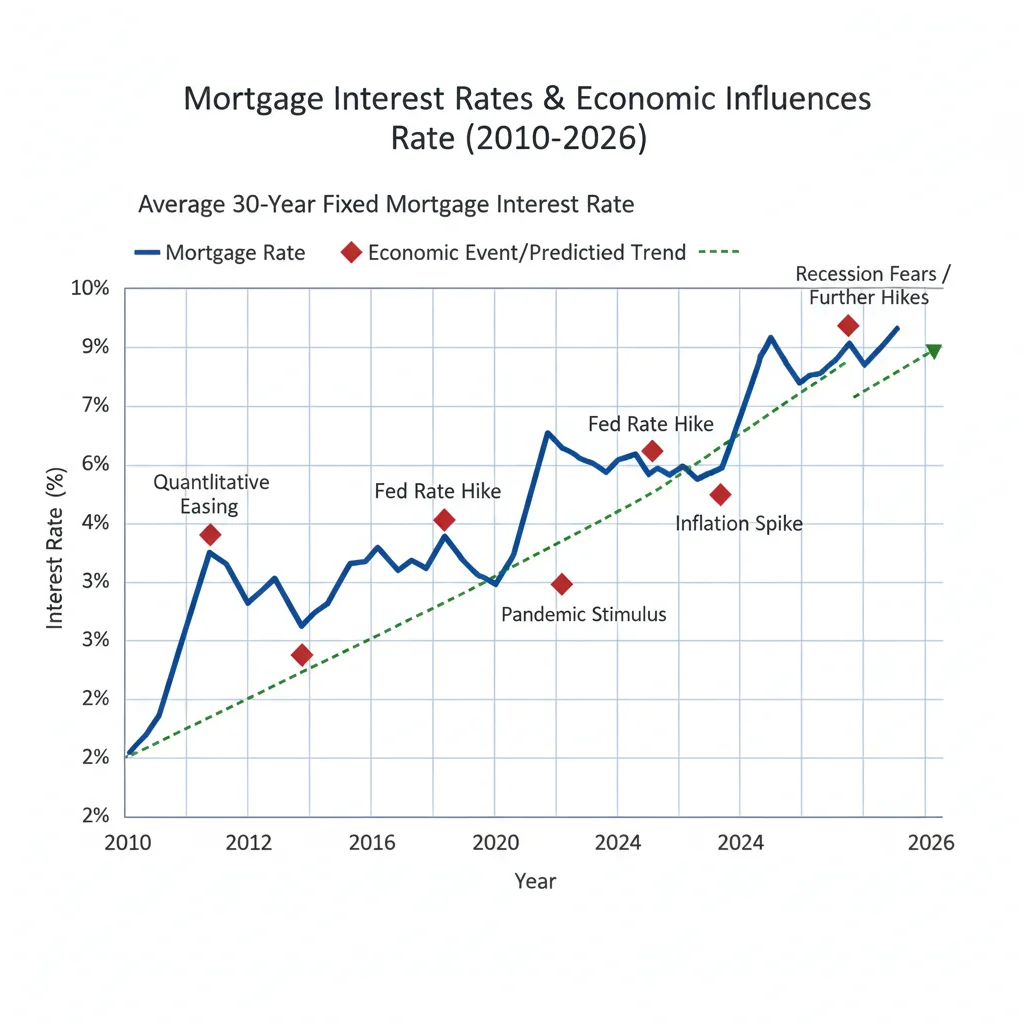

Before we project into 2026, it’s crucial to grasp the current state of mortgage rates and the forces that have shaped them. The past few years have been a rollercoaster, marked by aggressive monetary policy shifts by central banks in response to inflation. These actions have directly influenced the cost of borrowing, including mortgage rates. Understanding this historical context provides a foundation for anticipating future movements in personal mortgage rates.

Key Factors Influencing Mortgage Rates

Several interconnected factors dictate the direction of mortgage rates. These include:

- Federal Reserve Policy: The Federal Reserve’s decisions on the federal funds rate have a significant, albeit indirect, impact on mortgage rates. While the federal funds rate is a short-term lending rate for banks, it influences the broader financial market, including the yields on Treasury bonds, which mortgage rates often track.

- Inflation: High inflation typically leads to higher interest rates as lenders demand greater compensation for the eroding purchasing power of future repayments. The fight against inflation has been a primary driver of rate hikes in recent cycles.

- Economic Growth: A strong economy often correlates with higher interest rates as demand for credit increases. Conversely, an economic slowdown might lead to lower rates as central banks try to stimulate activity.

- Job Market Strength: A robust job market generally indicates a healthy economy, contributing to inflationary pressures and potentially higher rates.

- Global Events: Geopolitical tensions, international trade policies, and global economic stability can all create uncertainty, influencing investor sentiment and, consequently, bond yields and mortgage rates.

- Housing Market Dynamics: Supply and demand in the housing market also play a role. A highly competitive market might see lenders adjusting rates based on perceived risk and opportunity.

These factors are not static; they are constantly in flux, making predictions about Mortgage Rates 2026 a complex but necessary exercise for strategic financial planning.

Anúncios

Expert Predictions for Personal Mortgage Rates in 2026

Forecasting mortgage rates is an intricate process, with various financial institutions and economists offering their perspectives. While no one has a crystal ball, these predictions are based on sophisticated models and analyses of the aforementioned economic indicators. For Mortgage Rates 2026, a consensus is slowly forming, though nuances remain.

Potential Scenarios for 2026

Most experts anticipate a period of relative stability or even a slight decline in mortgage rates by 2026, assuming inflation is brought under control and the economy avoids a severe recession. However, the path to 2026 is unlikely to be linear. Here are some potential scenarios:

- Gradual Decline: If inflation continues its downward trend and the Federal Reserve begins to ease its monetary policy, we could see a gradual, moderate decrease in mortgage rates. This scenario would be favorable for refinancing activity.

- Plateau and Stability: Another possibility is that rates will stabilize around their current levels, or slightly lower, after central banks achieve their inflation targets. This would offer predictability but less opportunity for significant savings through refinancing.

- Mild Volatility: Unforeseen economic shocks or persistent inflationary pressures could introduce mild volatility, with rates fluctuating within a certain range. Homeowners would need to be agile to capture favorable moments.

- Unexpected Increases (Less Likely but Possible): While less probable given current projections, a resurgence of inflation or other significant economic disruptions could lead to further rate hikes. This scenario would be the least desirable for homeowners.

It’s important to remember that these are projections, and actual Mortgage Rates 2026 could deviate based on real-time economic developments. Staying informed through reputable financial news sources and consulting with financial advisors is crucial.

The Role of Inflation and Central Bank Actions

The trajectory of inflation will be the single most defining factor for Mortgage Rates 2026. If central banks successfully bring inflation back to their target levels (typically around 2%), the pressure to maintain high interest rates will diminish. This could pave the way for rate cuts, making refinancing more attractive. Conversely, if inflation proves more stubborn, rates may remain elevated for longer than anticipated.

Central bank communication will also be vital. Their forward guidance on monetary policy will provide clues about future rate movements. Homeowners should pay close attention to statements from the Federal Reserve, as these often signal upcoming shifts in the broader interest rate environment.

Refinancing in 2026: What Homeowners Need to Know

For many homeowners, the primary interest in Mortgage Rates 2026 revolves around the potential for refinancing. Refinancing can significantly impact your monthly payments, the total interest paid over the life of the loan, and your overall financial flexibility. Understanding when and how to refinance effectively is key.

When Does Refinancing Make Sense?

Refinancing is not a one-size-fits-all solution. It typically makes sense when:

- Interest Rates Drop Significantly: If Mortgage Rates 2026 are substantially lower than your current rate, refinancing can lead to considerable savings. A general rule of thumb is that a drop of at least 0.75% to 1% can make it worthwhile, but even smaller drops can be beneficial depending on your loan amount and remaining term.

- You Want to Lower Your Monthly Payment: Even if rates haven’t dropped dramatically, extending your loan term or switching to a lower fixed rate can reduce your monthly outlay, freeing up cash flow.

- You Want to Shorten Your Loan Term: If rates are favorable, you might consider refinancing to a shorter term (e.g., from 30 years to 15 years) to pay off your mortgage faster and save a substantial amount in interest over the long run.

- You Need to Access Home Equity (Cash-Out Refinance): A cash-out refinance allows you to tap into your home equity, converting it into cash. This can be useful for home improvements, debt consolidation, or other large expenses. However, it increases your loan amount and should be approached cautiously.

- You Want to Switch Loan Types: Moving from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage can provide stability and predictability, especially if you anticipate rising rates. Conversely, if you expect rates to fall further, an ARM might offer initial savings.

- You Want to Remove Mortgage Insurance: If you’ve built up sufficient equity (typically 20% or more), refinancing can allow you to drop private mortgage insurance (PMI), which can save you a significant amount each month.

Costs Associated with Refinancing

Refinancing is not free. There are closing costs involved, similar to when you first purchased your home. These can include:

- Appraisal fees

- Loan origination fees

- Title insurance

- Credit report fees

- Attorney fees

- Recording fees

These costs typically range from 2% to 5% of the loan amount. It’s crucial to calculate whether the savings from a lower interest rate or other benefits outweigh these upfront costs. The ‘break-even point’ – how long it takes for the savings to cover the costs – is a critical metric to consider when evaluating a refinance for Mortgage Rates 2026.

Preparing for a Refinance in 2026

If you’re eyeing a refinance in 2026, proactive preparation can make the process smoother and more advantageous:

- Improve Your Credit Score: A higher credit score translates to better interest rates. Start working on improving your credit now by paying bills on time, reducing debt, and checking for errors on your credit report.

- Reduce Your Debt-to-Income (DTI) Ratio: Lenders look favorably on lower DTI ratios. Work on paying down other debts to present a stronger financial profile.

- Gather Financial Documents: Have your tax returns, pay stubs, bank statements, and current mortgage statements organized and ready.

- Research Lenders: Don’t just go with your current lender. Shop around and compare offers from multiple institutions to find the best rates and terms available for Mortgage Rates 2026.

- Understand Your Home’s Value: Your home’s current market value will impact your loan-to-value (LTV) ratio, which is a key factor in refinancing eligibility and rates.

Beyond Refinancing: Other Mortgage Considerations for 2026

While refinancing is a major topic, homeowners have other strategic considerations regarding their mortgage in 2026, especially as economic conditions evolve.

Home Equity Loans and Lines of Credit (HELOCs)

If Mortgage Rates 2026 remain relatively high, or if you have a very low existing mortgage rate you don’t want to disturb, a home equity loan or HELOC might be a better option for accessing funds. These allow you to borrow against the equity in your home without refinancing your primary mortgage.

- Home Equity Loan: This is a second mortgage with a fixed interest rate and a fixed repayment schedule. It provides a lump sum of cash.

- HELOC: A HELOC is a revolving line of credit, similar to a credit card, where you can borrow money as needed up to a certain limit. Interest rates are typically variable.

Both options have their pros and cons, and the best choice depends on your specific financial needs and tolerance for interest rate fluctuations. The prevailing Mortgage Rates 2026 will also influence the rates offered on these products.

Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages

The choice between an ARM and a fixed-rate mortgage is always a critical one, and it becomes even more pertinent when considering future rate environments. If experts predict Mortgage Rates 2026 to decline after an initial period, an ARM with a low introductory rate might seem appealing. However, homeowners must be comfortable with the risk of future rate adjustments.

A fixed-rate mortgage, on the other hand, provides stability and predictability, locking in your interest rate for the life of the loan. This can be particularly attractive if you believe rates will rise, or if you simply prefer the peace of mind that comes with consistent payments.

Paying Down Your Mortgage Faster

Regardless of the direction of Mortgage Rates 2026, accelerating your mortgage payments can be a powerful wealth-building strategy. Even small extra payments can significantly reduce the total interest paid and shorten your loan term. This strategy offers guaranteed savings, unlike refinancing, which depends on market conditions.

The Broader Economic Landscape and Its Impact on Homeowners

The state of personal mortgage rates in 2026 is inextricably linked to the broader economic health of the nation and the world. Understanding these larger forces can help homeowners anticipate changes and plan accordingly.

Inflationary Pressures and Interest Rate Policy

The post-pandemic era has been characterized by elevated inflation, prompting central banks worldwide to implement aggressive interest rate hikes. The success of these policies in taming inflation without triggering a deep recession will be a major determinant of where Mortgage Rates 2026 land. If inflation proves persistent due to supply chain issues, geopolitical conflicts, or strong consumer demand, central banks may be forced to keep rates higher for longer.

Housing Supply and Demand

The fundamental balance between housing supply and demand also influences the market. A shortage of available homes can push prices up, impacting affordability and potentially influencing lending criteria. If housing inventory remains tight, even with fluctuating Mortgage Rates 2026, competition among buyers could remain fierce in certain desirable markets.

Technological Advancements in Lending

The mortgage industry is continually evolving with technological advancements. Online lenders, AI-powered underwriting, and streamlined application processes are making it easier and faster to secure a mortgage or refinance. These innovations can also lead to increased competition among lenders, potentially offering more favorable terms for consumers regarding Mortgage Rates 2026.

Strategic Tips for Homeowners in the Coming Years

Given the anticipated landscape for Mortgage Rates 2026, homeowners have several strategic avenues to explore. Proactive planning is always better than reactive decision-making.

1. Monitor Economic Indicators Closely

Keep an eye on key economic data releases such as inflation reports (CPI, PCE), employment figures (jobless claims, unemployment rate), and GDP growth. These indicators often provide early signals about potential shifts in central bank policy and, consequently, mortgage rates.

2. Regularly Review Your Mortgage Terms

Don’t set it and forget it. Periodically review your current mortgage rate, remaining balance, and loan term. Compare it with prevailing Mortgage Rates 2026 to identify potential opportunities for savings through refinancing or other adjustments.

3. Build a Strong Financial Foundation

Maintain a solid credit score, keep your debt-to-income ratio low, and build an emergency fund. These steps will put you in a stronger position to take advantage of favorable rates when they arise, whether for a refinance, a new home purchase, or a home equity product.

4. Consider Professional Financial Advice

A qualified financial advisor or mortgage broker can provide personalized guidance based on your unique financial situation and goals. They can help you navigate the complexities of Mortgage Rates 2026, assess the pros and cons of refinancing, and explore alternative strategies.

5. Don’t Chase the Lowest Rate Blindly

While a lower interest rate is attractive, always consider the full picture, including closing costs, your long-term financial goals, and how long you plan to stay in your home. Sometimes, the lowest advertised rate might come with higher fees or less favorable terms.

6. Explore Government Programs and Assistance

Keep an eye out for any government-backed mortgage programs or assistance initiatives that might emerge. These can sometimes offer more flexible terms or lower rates for eligible homeowners, potentially impacting your decisions related to Mortgage Rates 2026.

Conclusion: Preparing for the Future of Personal Mortgage Rates

The landscape of personal mortgage rates in 2026 is shaping up to be one of cautious optimism, with many experts anticipating a period of greater stability or even a modest decline after the recent volatility. However, the exact trajectory will depend heavily on the evolution of inflation and the subsequent actions of central banks.

For homeowners, this means that while significant opportunities for refinancing might emerge, especially if you secured your current mortgage during a period of higher rates, strategic planning and informed decision-making will be paramount. By understanding the key economic drivers, monitoring expert predictions, and proactively managing your financial health, you can position yourself to make the most advantageous mortgage choices for 2026 and beyond.

Whether your goal is to lower your monthly payments, reduce the total interest paid, or access your home equity, staying educated about Mortgage Rates 2026 is your best defense against uncertainty and your best tool for financial empowerment. The future of your home financing is within your control, provided you are prepared and well-informed.